How many times have you heard of those stories of woe and bankruptcy caused by the subprime lending and borrowing crisis, currently in the forefront of real estate market news? For me, too many. Here’s a typical account that I found in our local newspaper recently.

Well, there’s more where that came from: you don’t have to look too far to find more tales of struggle that echo the same theme over and over.

This is the type of stuff that could have repercussions across markets far and wide, and will be touching lives far and wide for years to come.

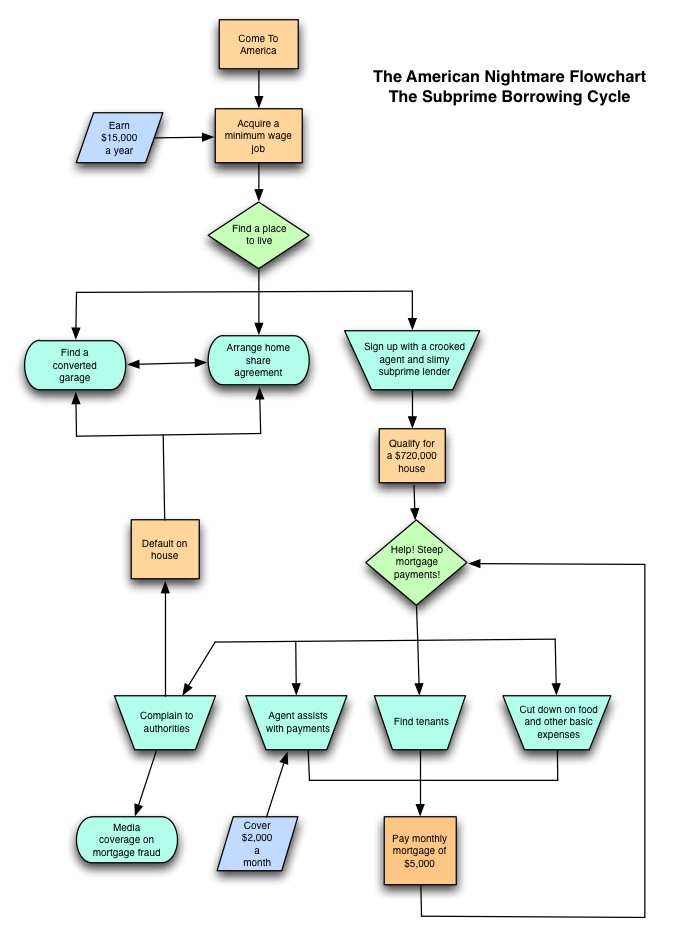

Ultimately, it all boils down to some typical scenarios that I’ve decided to illustrate in a graphical fashion. Following is an illustration that I’ve kept faithful to the actual stories of people caught up in this subprime lending mess (who are usually immigrants or lower income families). Everything here is factual.

Click here or on the image to enlarge it:

|

Don’t let your future end in an American Nightmare: stay away from those lousy loans! Sad to say, it’s already way too late for too many.

A Closer Look At Subprime Borrowing: A Case Study

Better to live in a garage than to live without enough to eat.

– Cristina Plata, subprime mortgage borrower

Now let’s segue into a case study that reflects how the American Nightmare typically unfolds.

With countless homes dotting the landscapes of California, all priced in the mid to high six figures (some even hitting $1 million), all on 5,000 or under square foot patches of ground, all with a maximum of 3 bedrooms and a couple of baths to make you feel like a “king”, how can you not attempt to get a piece of the property pie? How can you not help but play the real estate market like everyone else before you whose success you’ve coveted as well?

Seriously though, this is what a million dollars bought in certain parts of the nation, during the height of the housing bubble. Some of these homes are found in the outskirts of major cities in Northern California, some in flood plains or in baking desert-like surroundings.

|

|

|

|

During the height of the crazy real estate market, many new homeowners happily — no, desperately — made their first home buying purchase for such an abode. This may have been someone like Luis Mapula and his wife Cristina Plata, subprime mortgage borrowers and immigrants with 2 young kids who once lived in a converted garage and who tried to transition to a nice two bedroom house in East San Jose, California.

Back then, this fellow earned $54,000 a year working as a fence company construction worker, which by all accounts and especially by national standards, was a pretty decent living. But through a real estate broker, he found himself owning a ridiculously overpriced typical California home worth $543,000 with no money down. What’s surprising is that often, these people aren’t even in the market for a house to begin with and instead have been targeted by unscrupulous real estate agents. Many who are approached for home buying opportunities via these steep loans are people who have never heard of these schemes before, who are not financially savvy, who are the most vulnerable, and who are not familiar with how real estate is typically transacted. In the end, they are left holding the bag with ruined credit after perhaps struggling to pay for a mortgage that costs over and above their gross monthly pay.

How does this happen? Here is the usual chain of events that can happen to an unsuspecting victim.

The Subprime Borrowing Road To Broke

-

#1 Questionable real estate professionals begin targeting “customers”.

Sleazy agents frequent ethnic community areas to scout out targets. This would and could happen anywhere!

#2 If you are reading this list, you’re an unlikely target.

Targeted individuals and potential victims are often not native language speakers, and are enticed with stories of homeownership and the American Dream. The agents are relentless about contacting these people, reminding them of the opportunities that can be had.

#3 This is a case of too many real estate players handling an application.

A number of people work on the homebuyer’s applications and falsely inflate the buyer’s income to make them qualify for a house that is way out of their financial reach. This was how “liar loans” were concocted and born.

#4 Paying your mortgage can become a family affair or a rental business.

The homebuyers are encouraged to make their payments by doing creative things like renting out other rooms or pooling their finances with friends and family who may or may not decide to live under the same roof.

#5 Don’t look at me, I’m not the subprime lender!

When the fraud is discovered, usually when the homeowners get into trouble with their payments, the homeowners are then compelled to voice their complaints, which lead to rampant finger pointing among the accused real estate professionals. Involved agents will blame the subprime mortgage lenders for their “horrible loan programs that require little or no income documentation with low, teaser interest rates that rise dramatically after two or three years.” They’ll also fault the title companies or appraisers or anyone else they can shift the blame to.

#6 Fraudsters are playing a psychological game.

Scammers hope that the homeowner gets embarrassed enough not to sue or complain about what has happened to them. It’s a case of economic bullying.

Subprime mortgages and high rate loans are designed to help immigrants, low-income families and anyone with poor credit to purchase homes in heated markets. I find this whole concept quite incongruous, just like any kind of usurious debt scheme. When the market is heated, I always stay out of it. That’s been my philosophy all my life, so I deeply wonder why anyone with no money would want to buy anything when prices are going wild. I suppose that’s just how the system works: the types of loans that are made available to you when you lack the funds, become trendy and ubiquitous when demand is great and prices are sky high. We live in an amazing consumerist society that allows us to buy our dreams even if we are broke. But if I had no money, I’d be afraid to see how the dream could possibly end.

Better a garage than live without enough to eat, indeed.

Copyright © 2007 The Digerati Life. All Rights Reserved.

{kind=link}

{ 25 comments… read them below or add one }

That is a cool chart. It explains exactly what happens. Knowledge is Power so always read and learn about any industry you get into.

I think the important thing to realize is that no one cares about your finances as much as you do. Only we can know how much we can really afford. It is a sad thing that this sort of thing happens though, especially to those who are the most vulnerable.

-limeade

Nice flowchart. I was a bit concerned by the “Come to America” bit. Do you have any reference that shows that subprime borrowers are mostly immigrants?

OK, please ignore my earlier comment. I followed the sources of some of your links and there is more than anecdotal evidence for the link between minority immigrants and loan defaults.

Nigel —

That’s right, most victims of mortgage fraud stemming from subprime borrowing tend to be unsophisticated individuals not very well versed in the real estate market and the process involved. They are persuaded by slick and wily agents to enter into these high risk situations with the promise of the elusive American Dream.

Unfortunately, the world is filled with easy targets for scams and fraud; I just don’t see gullibility going away anytime soon.

Great Story and chart — oh so true. Homeownership is a serious proposition…

I agree that subprime lenders share some blame (if things are done fraudulently) but don’t people have some personal accountability? I mean, what’s a guy with $54,000 income doing in a $543,000 house? That’s just out of whack.

Vulnerability is one things, but stupidity is another. While laws can offer partial protection to the vulnerable, there are no known laws for stupid decisions.

Sometimes, the American Dream is just too enticing to turn away from when it is offered by who may seem like authoritative individuals who sound like they may know what they’re talking about. That’s how slick real estate agents appear to hard-working but naive folks who move here in pursuit of better lives. The sad thing is that the agents usually share similar backgrounds as their clients so there is a trust issue involved and this bond is used to coerce victims into participating in these risky schemes.

Some people just don’t realise that its not a good idea. I mean, if you are talking to multiple professionals who tell you that you can afford it, and someone is willing to lend you the money, why wouldn’t you believe them?

Three cheers to killing off unscrupulous lending policies, SVB!

There’s a loan type that’s actually designed as a trap which lots of regular folks got snagged in. Basically it lets you make a monthly payment that’s much less than your actual minimum mortgage payment (i.e. less than the interest-only amount). That money is tacked on to the end of the loan and you pay interest on it (negative amortization).

There are two really evil parts to the loan that make it a trap.

The first is that the lender would qualify you for the loan as long as you could pay the ridiculously low negative amortization payment — which was literally hundreds or thousands less than a regular payment.

The second is that the ridiculously low payment only lasted a year or so at which point the victim would have to try and pay for a loan they wouldn’t have qualified for otherwise.

These option-ARM loans (as opposed to regular ARM loans) have a big carrot upfront but make it easy for people to get taken-advantage of.

It’s one thing to be stupid, it’s another to see a number you can afford and not be told about the consequences 🙂

BTW, in California a person holding a real estate broker license can do real estate as well as mortgages. So in those cases, there’s often no finger pointing to be had and they can manipulate numbers to get their deals (both, big bucks!) to work.

What would be really interesting is if loan broker compensation were tied, not to the closing of the deal, but how successful the owners were at making their payments!

Steve, thanks for the valuable insights, especially from your point of view as someone in the profession. Do you feel that there’s almost this moral obligation that agents have when dealing with clients who are so stretched in this capacity? I’m wondering now whether agents make decisions as to whether or not to sell this kind of loan to their clients.

We have clients come to us after being taken advantage of by real estate agents and other lenders who’s only goal is to reap huge profits from the people and put them into a loan that paid the most for them. I think alot of mortgage fraud has originated from the bad agent or predator lender who wanted the money so bad that they just had the borrower “sign here”. Not too long after the borrower has been in the home do they realize that their payments are changing or their principal balance is increasing!

So true! This could be one reason why California mortgage lenders are doing good in the business. Preying on the minorities is quite unthinkable. If you think you are vulnerable, then you must be. Be vigilant. Ask around. Don’t be shy to do so. Like what Limeaid said, no one cares about our finances as much as we do.

This is unfortunate to be sure. The cost of homes is a premium in Hawaii as well! There are lenders here too that will give loans to just about anyone… if the interest rate is high enough. On the flip side of that, however, while the borrower may see them as little gods for rescuing a borrower when nobody else would loan them a dime, the lenders can actually be the ones in trouble. We have one in our little town whose parent company on the mainland just filed bankruptcy. They forgot about the part that those people with bad credit don’t always repair that credit and pay their loans back! I hate money, or at least the need of it the darn stuff! Okay, maybe not a garage but a quonset hut would be okay… I actually do like the sound of rain on a tin roof! 🙂

As has already been said, nobody is ever going to care about your personal finances much as you do. The government is currently looking at introducing some additional legislation aimed at tackling the way some mortgage brokers operate. Until then, it’s really important for people to be a bit more vigilant when dealing with mortgage and real estate brokers. That’s not to say that all of them are trying to shaft you but there are enough of them doing this that you should always be vigilant.

I am not a big fan of flow-charts, but this one paints a great picture showing the process and how easy it is for someone to be pushed off course by slimeballs.

Thanks for submitting this to the Consumer-Focused Carnival of Real Estate and we chose it as our winner this week.

Thanks for the great read!

Our Loan Compliance Advisory Group is committed to helping “Protect The American Dream.” We are dedicated to helping Homeowners Nationwide, that may be victims of Deceptive Lending Practices.We are open for any suggestions on how we can help.

Several members of our Loan Compliance Advisory Group attended the “March on Wall Street.” We support the “Save Our Homes/Restructure Loans” important message that Rev. Jackson and his dedicated coalition members are spreading across America. The December 10, 2007 rally, one of several recently held across the United States, sponsored by Rev. Jessie Jackson’s Rainbow PUSH Coalition, the National Association for the Advancement of Colored People and the Urban League, was a magnificent well planned informative event.

Wow. This post was remarkably prescient.

Today we have a buyers market and an economy in the toilet which is why so many people find themselves stuck. I hope that the Obama adminstration can straighten out this mess and set this country back on the road to economic recovery.

Don’t let any lender try to talk you into borrowing more money than you need or can afford. Make sure to take your time and don’t feel pressured or rushed. Beware of any nothing-down loans and altered information to qualify you for a home loan. Don’t borrow any money that you can’t afford to pay back.

We all need to watch out for others who want to take advantage of us.

Subprime loans definitely played their part in the entire credit crunch and housing market crash but at the same time people must be accountable for their actions. If the bulk of the population realized the lifeblood of their financial health depends on their credit score, many would realize it’s much easier, cheaper and smarter to simply hire a professional credit repair expert. Before studying the craft I hired an excellent company who helped me go from the low 500′s to mid 600′s within 3-4 months.

What we need now is our politicians to get back to reality and and stop buying themselves into office. Government policies are defying the basic logic of how money works.

I knew my son could no way qualify for the loan his real estate agent (a broker) enticed him to sign on the dotted line. However, somehow he “qualified” by someone messing with the “paper work.” It seems to me my son should go after the real estate agent for damages. Some will say: Well the fool should never have signed on the dotted line.” But I say, that is not my issue.