Before answering these questions, let’s touch on a few investing basics. Whenever you consider any investment, it’s crucial to investigate how the holding fits in with your risk tolerance and goals. Bonds are considered less risky or volatile — meaning their price movements vary less than those of stocks. Conventional investing wisdom recommends that by adding bonds, you can reduce your portfolio volatility substantially.

Bonds can reduce your investment risk, but should you invest in them now? Before answering that question, you need to have an asset allocation in line with your personal risk tolerance. If you’re going for a higher return, you must take on more risk for the opportunity to achieve that greater payoff. Bonds are an important part of an overall portfolio strategy. After you determine your preferred asset allocation, then it’s time to fund the bond or fixed portion of your portfolio.

At a high level, you can help determine your bond allocation by using a basic and simple formula. This formula can provide an approximate reading of what your non-stock allocation should be — that is, it may give you a hint or some idea of how much of your investments should go cash or bonds vs equities. Here’s the formula:

100 – [your age] = your stock allocation

For instance, if you’re 40 years old, you can start off with a 60% allocation for stocks (100 – 40), thereby making your cash and bonds allocation around 40%. This approach is not set in stone, but is rather a guide that you can use to figure out what allocations to make.

Individual Bonds vs Bond Mutual Funds

All bonds are not alike. Bond investments range from the most secure one year government Treasury bill yielding less than 0.17% as of early 2012, to longer term junk (or low rated) bonds averaging above 7% at this time (e.g. check out the JNK ETF). The investor can purchase individual bonds and hold them until maturity, at which time the face value will be returned to the investor. For example, buy an A rated 5 year investment grade bond at par for $1,000.00 and receive yearly coupon or interest payments of 2.5%. Go longer term on your investment horizon and the 20 year A rated bond will pay 4.35% on average. If you sell the bond in the secondary market before maturity, you may or may not receive your original $1,000.00 principal payment back. Furthermore, unless you have at least $30,000.00 or more to invest in bonds, it is difficult to get enough diversification in your portfolio when investing in individual bonds. So, individual bonds in and of themselves, have some draw backs.

What about a bond fund? The advantage to investing in a bond fund is that you get great diversification for a reasonable amount of money. Additionally, there are multiple varieties of bond funds, suitable for any investor’s preference. But unlike investing in individual bonds, funds do not have a maturity date. Put your cash in a bond fund today, and when interest rates rise, your principal investment value is certain to fall. Long story short, when interest rates go up, you’ll lose money when you sell.

Bonds vs Stocks: Long Term Investment Performance

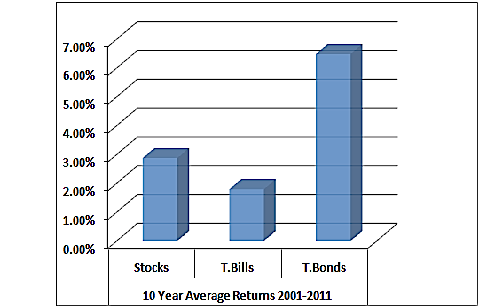

Anyone over the age of 30 is familiar with historical bond interest rates. In fact, over the last 83 years, the annualized average stock returns were 9.23% and Treasury bond returns were 5.14%. So how do you reconcile that history with the more recent inverted returns of stocks and bonds? During the first decade of this century, bond returns far surpassed those of stocks.

Historical Annualized Returns

|

As you can see, for the past ten years, stocks returned a measly 2.88% while lowly government bonds returned an unusually stout 6.49%. The recent returns are inconsistent with the long term asset class returns.

How is an investor to predict future returns and organize his or her portfolio with such conflicting data? Let’s understand why bond returns have soared.

When interest rates fall, bond prices rise, and vice versa.

Treasury bill interest rates, the barometer for the interest rate market, have fallen substantially over the last few years. In 2006, the one year Treasury bill rate was at 4.68% while in 2011 the rate fell to 0.03%. There’s no magic here. The infallible bond return and interest rate relationship held true. Interest rates fell and bond returns rose.

It’s highly unlikely that bond interest rates will drop any further; in fact it’s practically impossible. How much lower can they drop from 0.03%? Given bonds’ inverse relationship with interest rates, if you invest in a bond or bond fund now, then when interest rates increase, the value of your bond holding will decline.

The Yield Curve and Bonds

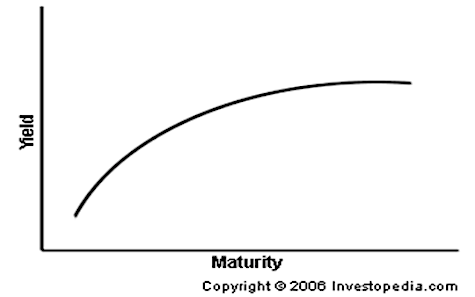

The yield curve is a graphical representation between bond yields and time. At any point in time, a yield curve can be created for any type of bond; it plots short and long term interest rates along the X axis, while yield (or interest rates) is found along the Y axis. The yield curve informs the investor about professional bond traders’ views of the future of the economy. Research has shown that the yield curve is helpful in making economic forecasts.

A steepening and upward yield curve suggests that the economy is expanding as monetary policy invigorates the economy. As the economy expands, corporations’ profits increase, stock prices rise, and investors usually flock to equities in order to participate in their growth. If the economy begins expanding too quickly, the government may raise interest rates to temper the economic growth. Further into an economic expansion, as interest rates rise and bond prices fall, investors tend to increase their bond holding to capture the higher yields.

A flat curve foretells a slowing economy. The inverted or downward sloping yield curve forecasts at best, an economic slowdown and at worst, a recession. In fact, every recession since World War II has been preceded by a downward sloping yield curve.

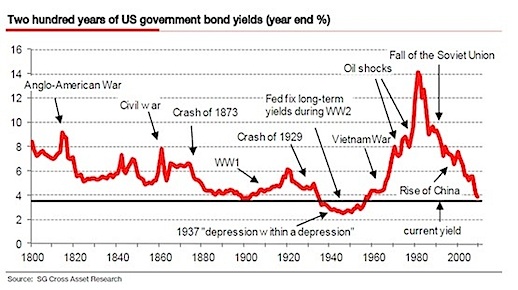

This chart, depicting 200 years of US government bond yields (through 2006) shows that we are at unprecedented low levels of return for bonds. Remarkably, world events caused small declines in bond yields in most cases, although not all. As previously stated, the most important driver of bond yields are interest rates. When interest rates rise, so do bond yields. Conversely, when interest rates are low, as in the current environment, bond yields are low. Watch out when rates begin to rise; although you will be able to snare higher interest rates on new issues, the existing bonds in your portfolio will certainly decline in value, with the longest maturities, falling the most.

How to Invest in Bonds Today

Now that you understand basic bond investing, here are some recommendations for the bond portion of your portfolio.

1. Buy individual bonds and hold until maturity. If you have a larger portfolio and can afford to diversify among several individual bonds, this strategy can protect your principal investment. For example, if you have $30,000.00 of investable assets for your bond portfolio, then you can invest in individual bonds. Consider a few corporate bonds with varying maturities from 3-7 years. Throw in some Treasury I (inflation protected) Savings Bonds and you have a reasonably diversified bond portfolio. Plan on holding the bonds until maturity and protect your principal. If interest rates rise, you will not have to sell at a loss. By varying the term of the bonds, if interest rates are higher when the 3 year bonds mature, then take the principal and reinvest in a higher yielding bond. If you purchase a lower rated bond, you can boost your yield a bit. Just realize that when the credit rating declines, the risk of issuer default goes up.

2. Don’t have much to invest? Put your entire investment portfolio in Treasury I Bonds with varying maturities. You are certain to protect your principal investment and the return will rise if inflation kicks up. You may also consider investing in TIPS or Treasury Inflation-Protected Securities.

3. The only bond funds to consider now are those with exceptionally short term maturities. You won’t get much of a yield, but you shouldn’t lose too much principal value when interest rates rise.

Making Bond Buying Decisions: Is Now a Good Time to Get Into Bonds?

Given that interest rates are at historical lows and the principal value of your existing bonds will decline when interest rates rise, the answer is… it depends. If you plan on holding the bonds until maturity, now is a fine time to invest in bonds. If you expect to sell the bonds before they mature, this is a bad time to invest in bonds. If you are considering investing in a bond fund, with the exception of extremely short term bond funds, be prepared for the value of your bond fund to decline when interest rates rise. Why not hedge your bets and invest incrementally in bond investments over the next few years?

Barbara Friedberg, MBA, MS is editor-in-chief of Barbara Friedberg Personal Finance.com where she writes to show you how to build wealth. Learn about personal finance from a real life Portfolio Manager & university professor! Stop by the website, subscribe to the FREE Wealth Tips Newsletter and get a free bonus eBook, 20 Minute Guide to Investing.

Created June 7, 2007. Updated February 27, 2012. Copyright © 2012 The Digerati Life. All Rights Reserved.

{ 12 comments… read them below or add one }

Once upon a time, we had bonds.

While stocks tanked in early 2000, we had good representation in bonds which provided strong returns for a while. This part of our portfolio we subsequently shifted back to cash as we reacted more conservatively — thinking there would be better opportunities for this money later on. We thought it would be best to accumulate and require this cash cushion after we took more risk in the business front and ended up with less job income in the last year. But it turns out that we may have miscalculated our reality somewhat, causing us to play it more safely than we should have. Our cash cushion has grown a bit too large for our taste, yet we’re not willing to take an enormous amount of risk with it. As mentioned, one of our options is to review whether bonds are something to look into, to reduce risk in the long term. From cash to bonds, we’d be trading one form of risk (that of inflation risk) for another (that of slight volatility inherent in the bond market).

We wonder whether bonds are a good bet at this time. At the time of this writing, we have an inverted (or flat) yield curve, which shows that we would probably be better off picking shorter term bonds. If we get into bonds, we’d only put in 10% at most as we plan to redistribute our cash elsewhere, at some point. But if we consider 10% in mostly short term bonds, why even bother? Why not just remain in our trusty tax exempt money market fund which is now currently yielding 3.77%? This is a good deal because our taxable equivalent yield is around 6%, and we get this yield with practically no risk!

As you can see, we’re a bit confused as to what we should do.

Ultimately though, if we were to get into bonds now, it’s more for diversification purposes, in case those rates start to slip down the road. Are we sacrificing that safety and security for the opportunity to hedge? It seems like a wash if you compare short term bond yields to current cash account yields but these similarities may not last that long and it’s the future we’re not sure about. As people who have hardly ever owned bonds in our past lives, I’m not particularly sure if we’re going to gain much out of doing such a shift from cash to bonds these days, but convention is telling us to do it given our age.

Maybe it’s not really worth all the fuss. After all, we’re not talking about emerging market stocks here!

How about you? Would you move out of a fairly safe money market fund that yields an equivalent 6% taxable return and into an intermediate or short term bond fund? The answer we’ve arrived at for now is yes: again, we’re doing it for the sake of diversification and not to chase current rates.

Well if you recall in your past article that showed how our portfolios look, I am a big advocate of bonds provided that they are the right kind and used for the right reasons. I currently hold about a 35% bond position (through a few mutual funds) and it is keeping up with and/or beating the S&P.

There are two reasons I like bonds. First, they produce steady income. This is good because this regular income can then be used to further enhance your portfolio by re-investing those proceeds. Unlike stock positions you aren’t relying on capital appreciation for growth so you can keep your principal in bonds relatively steady and that income that is generated is just like adding more money to your account.

The second is the downside protection/diversification which you mentioned. If you have a bond position that is yielding 5-6% and the equities are flat or even down you are reducing your losses and with the DCA of bond income you can potentially help boost your portfolio over the long term.

As long as your bond position doesn’t consist of strictly government or lower yielding AAA bonds, they should have a positive effect on your returns. So if you go for slightly more risky bond holdings you should be able to see decent returns.

Of course that’s just me 🙂 Bonds always seem to be thought of as very conservative, safe and low-yielding investments used to reduce risk in a portfolio but there is a lot more out there.

Have you considered building a CD ladder too? My local (Georgia) credit union has CD rates for 1-3 year CDs with 5.25% APY. I (age 35) lean towards a higher stock % than you, but do have CDs too. The REITs are another good move I agree with as part of your non-stock holdings. I believe stocks will give you a better return with such a long time horizon still than bonds though.

Indexes that track commodities, currency carry trade also would be good non-stock classes to look at.

I’m not very confident in that taxable equivalent yield of 6% figure. I bet that calculator is using Marginal tax rates rather than effective tax rates. I know my effective tax rate is about half my marginal tax rate, and when I use the effective tax rate to compare yields, the munis are not nearly so attactive.

I’ll say more later…

FYI

http://www.fool.com/personal-finance/taxes/2007/03/02/your-tax-rate-marginal-vs-effective.aspx

For what it’s worth, I think dividing the fixed income part of your portfolio between cash and bonds in the best idea. While it is true, that money market funds yield more right now, for the 12 months ending 5/31, the Vanguard Total Bond Mkt Inx returned 6.59% and the American Century International bond fund returned close to 8%. So something is up with bonds.

This is may own target asset allocation:

10% Vanguard Money Market fund

10% Vanguard Total bond market index

10% American Century International Bond

8% Vanguard Inflation protected bonds

7% DB G10 Currency harvest fund (DBV)

40% Globally diversified equity funds

5% Timber REITs (RYN, PCL)

10% Precious metals ETFs (CEF and SLV)

Very interesting guys. I think I’m going to mull this over further and definitely get into a better bond allocation soon, although the markets are a little roiled right now. I’m going to see about the riskier bond scenario as well, while international bond funds look appetizing too. If anything I’ll probably munch.

We also checked out currency hedging but so far haven’t decided to include it in our allocation; we thought instead to increase our foreign equity exposure figuring that it may deliver the same hedging effect for us. If you have further thoughts and details on this, I’d love to hear it!

Lots has happened since we first wrote up this page, but we’ve updated our information since then and we’re putting things in a new perspective. We’re ready to review bonds in the current rate environment.

Also, it’s been pointed out that as opposed to what I’ve mentioned in my first comment, the yield curve is actually gradually upward sloping right now.

Does anyone care that while the NAV for bond mutual funds falls with rising interest rates, the yield rises as well? Perhaps bond mutual funds work best if one doesn’t want to treat it as a stock

Lots of great bond discussion. I’m partial to splitting the fixed portion of my asset allocation between cash, inflation protected bonds and corporates. In this environment, laddering (varying the time to maturity) is quite important. If you get into a long term bond fund now, be prepared for a decline in long term principal values when interest rates rise.

And, as Chris implied, leave some cash on the table to deploy when bond yields rise.

@Barb,

What do you think about the Fed’s stance and commitment of keeping rates low until 2014? It may be a while before rates go up, unless something unexpected disrupts the status quo.

@SVB, I think it is part of their overall plan to encourage economic activity. By keeping rates low, corporations can borrow money at low rates and further their growth and expansion strategies. Additionally, consumers may benefit from low interest rates and low housing prices and participate in this unique housing market. Historically, low interest rate environments are accompanied by economic growth and increasing stock prices. The economic community is split on the efficacy of this strategy. I hope it works to get us out of the economic slump.

Meanwhile, I’m refinancing our home with a 15 year mortgage to personally take advantage of the low rates.