Here’s the latest update on our investment returns: our stock allocation is down 50% YTD, though our total portfolio is “only” down by 28% YTD, thanks to asset allocation and stock market diversification methods.

It occurred to me that it’s been a while since I’ve given an update here on our personal investments, though I’ve mentioned just how much we’ve been affected (like everyone else) by the stock market volatility. It’s nerve-wracking for me and my spouse, since we rely on our investments as our safety net, for the psychological reassurance that “things will be fine” while we don’t have stable incomes and are taking risks in our work lives.

Of course, as Murphy’s Law dictates, the year we dared take risks with our cash flow by leaving the 9 to 5 workforce behind, is the same year that our investments and savings decide to take the worst dive in our investing lives. The tiny consolation? Selfish as it sounds, it’s that we’re not alone in this misery. Being mainly index fund investors, we face a situation that isn’t unique, and as far as returns go, our financial numbers aren’t far from the norm.

Although I’ve said it in the past, let me reiterate that the stock market bear has REALLY claimed our portfolio. Here’s a snapshot of our portfolio numbers, captured sometime at the end of last year.

Our Total Portfolio’s Latest Investment Returns: Stocks Down!

| Asset Class | ~ One Year Return (Oct 2007 to Nov 2008) | Returns since July 2008 |

|---|---|---|

| U.S. Stocks / Taxable | -50% | -40% |

| U.S. Stocks / Tax-Advantaged | -57% | -48% |

| U.S. Stocks / Nasdaq | -47% | -41% |

| Foreign Stocks / Taxable | -54% | -46% |

| Bonds | 7.50% | 2.5% |

| Cash | -8.3% | 5.67% |

| Total Portfolio Returns | -38% | -28% |

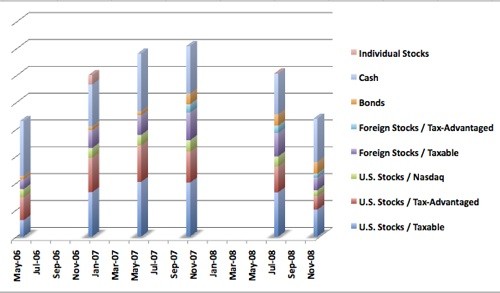

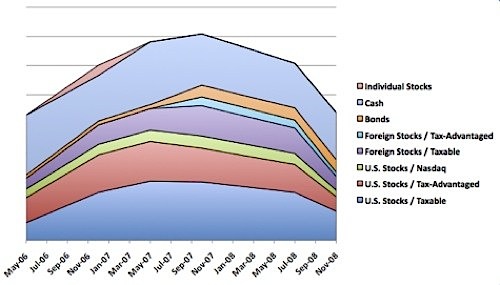

I’ve also updated our historical investment charts to display the sharp drop in our total portfolio returns as seen in comparisons between our July 2008 numbers vs those taken from late November 2008. You can see that any gains we made in the last 2.5 years have evaporated altogether. Easy come, easy go.

Our Historical Portfolio Returns: Bar Chart

Our Historical Portfolio Returns: Area Chart

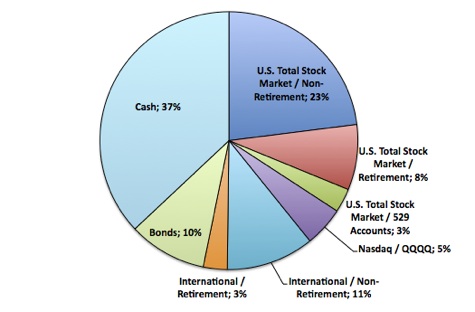

Because of the incredible shrinkage experienced by our equity positions (in domestic and foreign stock funds and ETFs), our asset allocation is now significantly altered and looks quite different from how we had it just a few short months ago.

Our Asset Allocation Is Out of Sorts

Our total equity allocation has drifted off by 12% from how we had it set up previously — it’s now diminished by 12% from our original allocation. From around 65% of assets in stocks, we’re now just 53% in stocks. Our bond portion used to be just 7% of our totals, but currently represents 10% of our portfolio; while cash now occupies a huge 37% allocation, up from a former 25% representation. Clearly, our asset allocation is completely out of whack, and will need to be reworked and rebalanced quite a bit.

We’re also taking this opportunity to rethink our allocation, and we’ve decided, as a couple, to tone down our investments ever so slightly. Based on our ages (and our discovery of what our true risk tolerance is….), we’ve now decided to trim our stock allocation by 5%: from 65% down to 60%. I think it’s an appropriate change. We’ll raise our bonds up from 10% to 15% while putting some of our cash to work in the stock arena, to balance things out. In the future, we’re planning to buy some REITs and possibly gold for some diversification, although we’re not in a hurry at the moment.

Our Asset Allocation Gone Awry

I think the time is ripe for a great big allocation overhaul. The stock market seems to have calmed down a bit and has tempered itself. It looks like a stock market bottom is potentially being formed, through ongoing backing and filling. Hopefully, the market is setting the ground for a new foundation that will lead to an improved investment climate.

I think now is as good a time as any to rebalance our allocation. We’ll just need to be careful that we don’t take too much out of our cash savings to perform this readjustment, since we need a lot of that cash to help cover our household’s temporary budgetary shortfalls over the next year.

How are you dealing with your investments these days?

Copyright © 2009 The Digerati Life. All Rights Reserved.

{ 15 comments… read them below or add one }

Our portfolio has gone down in the same range as yours for 2008 – around (-35%). We are currently in the process of re-balancing our portfolio and reconsidering our asset allocation. Looks like we’ll go for 65% stocks, 30% bonds and 5% cash. We will write in details about the final details at our blog :)). We are positive that things can only improve from here onwards. So lets keep our fingers crossed.

SVB,

Great detailed analysis.

I have to ask a dumb question. How did you lose 8.3% in cash from 10/2007 to 11/2008 – a bad money market fund, or did you forget where you buried a suitcase full of money? 🙂

Thanks for asking SS,

Actually, we’ve been living off our savings a bit over the last couple of years. Also, we’ve been using a good chunk of change to fund my husband’s startup. Both he and I are self-employed and have been working on bootstrapping our businesses and that’s where some cash has been used. I’ve mentioned in a few posts that our main goal right now is to become cash flow positive as soon as possible! Again — lots of risks to undertake during a recession….

Doesn’t changing the AA to reduce equity exposure _right after_ a huge downturn defeat the whole point of “pick an AA and stick with it by rebalancing”?

Dangerman,

Thanks for the great question. We have very good reasons for making a tweak in our allocation. The main thing to know is that this is not entirely an emotional decision — if it were up to me, we’d be more aggressive about our plans here. First, the change is not significant, and we had been planning this for a while now, so it’s not a big surprise.

Second, it’s about risk management, and I’m not talking about investment risk. We want to preserve our cash to support a startup and our living expenses. We can’t afford to move everything into stocks right now and increase our risk by doing so. By rebalancing, we’ll advertently have to use some of our cash, but we need the liquidity to sustain ourselves. We want to protect our emergency fund here.

Lastly, if you knew how truly old we are, then you’d understand 😉 . I believe that an AA strategy doesn’t have to be rigid. You’re entitled to making some adjustments based on your life situation, conditions or other factors. For instance, some people I know tilt their AA towards more stocks when they feel more optimistic about the future (adding 5% more toward their stock allocation than they normally would, during certain times).

might want to add some gold to your portfolio and some commodities as well. Every diversified portfolio should have some. But I think your asset allocation makes sense now.

Mr CC,

I was actually thinking of adding 2.5% gold and 2.5% commodities in the whole mix, although if you look at how prices have been these days, it wouldn’t have been a great call to have held on to these asset classes. I am also thinking of jumping into REITs, but they’ve literally fallen from the sky lately and it would be like catching a falling knife. Of course, you’ll say that this is some form of market timing albeit the long term kind, but given the rout in all asset classes, it’s hard (emotionally, not strategically) to make the commitment to jump in when things are so pessimistic (we’re still waiting to see what the fallout would be on the bailouts…).

I am pretty comfortable with equities and stocks though, having been a stock investor for 2 decades, so rebalancing into stocks has never been an issue for me; it’s more to do with trusting how other asset classes are expected to behave in the long term (e.g. precious metals, real estate, commodities).

My investments also took a 35% hit. I did manage to put half of one (financial sector) into cash before the big drop occurred in October 2008. I’m still staying the course with my other investments. I’m 25 years from retirement so I know I will get opportunities from the rebound. I, like you, believe we’re nearing the bottom (fingers crossed).

Your returns are very similar to our own.

If you are not comfortable taking a large, sudden position in new asset classes, maybe you should consider making small purchases over time. That would allow you to get in REITs and commodities slowly and without buying into a sudden price drop.

I am investment advisor, but you cash position seems awfully big.

I’m feeling pretty smart about now for getting out of the market at the beginning of last year when I heard about the whole housing market thing. I have a feeling I am going to do something real stupid soon though and lose more than I saved by not being in the market. 🙂

I agree, asset allocation has to change as you age and as you become a more seasoned investor. What if your initial allocation was wrong? I’ve realized that I was overweight in stocks and under weight in bonds, I’m not making drastic changes but I am working to balance a bit better. This is with an eye on the long term, not the short term. I’m a little late to that party.

Diversification is the name of the game, it sucks to see -50% but you have to take the good with the bad.

Good thing you diversified! It would really be painful if everything lost 50% (worst yet, if your life savings was in AIG or something).

David (MoneyNing),

We’ve got a very close friend who put a lot of his money into Freddie Mac at a price of $60+ and he eventually bailed out completely at $0.70. He said that most of his money was tied to this investment. Ouch. I cannot fathom what effect this has on his situation today.

Part of the reason markets can fall 50% from peak to trough is that people sometimes allocate away from whatever has done down the most, and towards whatever has gone up the most. How many people decided in 1999 that ‘Internet’ was a sector worth a 5-15% allocation in their portfolio, only to change their mind in 2002 and sell at the bottom? By definition: lots. Prices can only reach a bottom when people are done selling.

It’s good that your allocation change was moderate, though — I second the question about cash. Why not something like 70% stocks, 20% bonds, and 10% cash? I can’t think of any scenario — short of something almost literally apocalyptic — in which a shift from cash to bonds doesn’t raise your return without doing much to your risk.