What has Michael Jackson got to do with my money?

I’m in a retrospective mood, so I thought I’d share with you a couple of stories about my earliest experiences in the stock market. There’s been such a stark juxtaposition between some of these experiences that I thought it was well worth discussing. When you look back at how you first made a thousand dollars from the stock market or how you first lost a few thousand, do you notice the type of circumstances that surround these events? I never realized how much of a “cliche” these stories now seem to appear when you’re analyzing them after the fact, but in reality, I’ve noticed that when dealing with the market, the same patterns of behavior would yield me fantastic results, while other actions quickly result in financial loss. Looking back, these were lessons I probably couldn’t have learned any other way.

How I Lost My Shirt In The Stock Market

After graduating from college, I found that I had $12,000 in the bank at that time, thanks to my first job and after scrimping and saving throughout my school years. I had built up my savings from odd jobs, internships, gift money and allowance money I’d received up to that point and it took all of the first couple of decades of my life to get there. I recall that first year on the job at a quickly growing company that developed database software — and it wasn’t just software development I was interested in learning about. Since some of the perks of this company also included a small number of stock options, a 401K plan and an ESPP plan, I sought to understand how the stock market worked and thus opened a discount brokerage account.

That time, the stock market was doing very well and since my options and ESPP account were gaining ground, I thought I would put my other $12,000 to good use. I had been closely guarding this money by placing it in a money market fund while I figured out what to do with it. Various financial magazines I’d been reading (such as Kiplinger’s Personal Finance known then as “Changing Times” and Money Magazine) were touting individual stocks among other investments, and one particular stock recommendation caught my eye. That year was the year of L.A. Gear, a hip sneaker company with a high flying stock that just snared an ad campaign starring who else but the “King of Pop”, Michael Jackson!

And you can guess this one coming a mile away: L.A. Gear’s stock (OTC symbol: LAGR) was over $30 at that time at an all time high, and had a chart that showed a sharp upward trajectory that had unfolded in recent months. Jackson was on television heavily promoting the brand. I ordered shareholder information from the company to study its prospectus and find out more about this opportunity. The ongoing media blitz and rapidly rising stock price convinced me that things could only get better for L.A. Gear, and I became certain that I could never lose…so I bit. In a big way. It would be impossible for me to lose, since I’d been doing my homework.

How can I not be mesmerized by their fabulous commercials (oooh, Paula Abdul is IN!)?

So I bought close to 400 shares with my $12,000 at $30 a share in the summer of 1990. That June I committed what you may call my life’s savings to L.A. Gear and Michael Jackson. 😉 In a month’s time, that $30 would not make headway. The stock price was at its peak and refused to budge upwards. Eventually it would slip to $28 and would swing in price from $28 to $29 a share all the while frustrating and aggravating me as I saw my account go through a gradual decline.

But that decline would not be gradual for long as August of 1990 rolled in, along with Iraqi war tanks into Kuwait. The Kuwait invasion made headlines, and the whole stock market turned terribly sour for a few months. My “investment” in this individual stock promptly plummeted and as I watched it go lower, I kept reassuring myself “it’s just a blip, it should come back up.” I also thought that as soon as the stock price recovers and goes back to my original buy price, I would get the heck out of my position. This seems so predictable, but it’s how we all think once the market turns against us. We all just want to get our money back whole.

Instead, the price went lower and before long it was at $15 a share and I couldn’t take it anymore. So I sold out, took a loss and recovered all of $6,000 of my original investment.

I will never forget that souvenir of the Persian Gulf war experience that I “took home” with me. While the rest of the stock market recovered from the short-lived volatility and begun an upward trend that would last a decade, L.A. Gear failed to ever revisit its peak, which was coincidentally — as Murphy’s Law would dictate — very close to the price point I had bought at. Several years later, the stock eventually hit $0.

Of course, I’ve made more stock market mistakes since then, but none as resounding as this one, from which I learned to “not put all my eggs in one basket”, especially when it came to individual stocks.

How I Got My Shirt Back and More Through The Stock Market

On the flip-side, you may be interested to hear how I made my first $100,000 in the stock market, or rather, how I made back the money I lost…and more. Well, it’s a story that pales in comparison to how I lost my first several thousand dollars. But it all starts with the leftover $6,000 I managed to recover from my first and biggest investment loss (percent-wise), which was as nasty an experience as they could come. I’m sure you’d agree that a loss of 50% of your savings in 2 or 3 months’ time can be called pretty dumb.

But at that point, I vowed to make up for the loss and I began to try out mutual funds. Once more, I looked to some great investment brokers and mutual fund companies to offer me selections. I became “gun-shy” about participating in the market during that crazy period between 1990 and 1991 so I decided to dollar cost average my way in using whatever money I had left and the disposable income I had from my entry level tech job.

I proceeded to put in $500 a month into a variety of Janus funds and before I knew it, a couple of years had past and I more than made up my money (albeit mostly from the monthly savings I put in religiously into the funds). Here’s how it worked:

My monthly investment was $500.

The rate of return was over 10% (though I cannot remember what it was exactly).

The total amount I invested was $12,000 in 2 years.

The value of my investment was then around $13,400.

This helped bolster my confidence that I could actually make up for lost ground. I continued to make regular investments through retirement funds and using any increases in my disposable income to add to my accounts. All I remember was that in a few more years, I had eventually hit $100,000. Here’s another illustration of how that happened:

My monthly investment was raised to $1,000.

The rate of return averaged at least 10% (again, this was during the strong market years of the 1990’s).

The total amount I invested turned out to be $60,000 in 5 years.

The value of my investment rose to somewhere between $80,000 and $100,000.

Sure, it took a little bit more time to get to a 6 figure investment account, but I finally made it to that point. The system I followed to get to this point was much more strategic, consistent and AUTOMATIC. I also did it without expecting massive returns in a few months’ time and I promised myself not to get ahead of myself trying to assume more risk than necessary. I thought about how happy I would be if I could just get my money back without it taking forever to do so. Well, I was surprised it didn’t take that long (despite how gains were made gradually) and that it took only meeting the market averages to make it work.

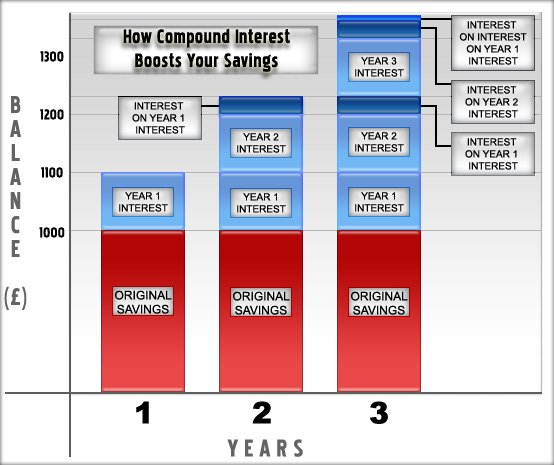

I must credit the effect of compounding on my investment returns for this success.

These days, I confine my individual stock investments to under 4% of my entire portfolio, while making sure the rest of my portfolio tracks the indexes. Because of the phenomenon of compounding, you can bet that a 6 figure account is well on its way to 7 figures just by sticking to this path. There’s magic here alright, and it’s not coming from Michael Jackson.

Final Thoughts

As you can see, it took me only 3 months to lose half my life’s savings “playing” the market. And it took me another couple of years before I made it back. But continuing down the new path with mutual funds and systematic investing has made me many times more money than I’ve ever lost. It goes to show that the stock market provides the best rewards for any investor when it’s approached with care and caution. I no longer have the urge to swing for the fences (although once in a very rare while I may take additional risks with a very small portion of our portfolio), and our investment emphasis is for modest growth with capital preservation while we nix the aggressive, high-risk investment pursuits. We’ve been happy with the results of our basic approach to stock market investing — yeah, despite the comments I get here from time to time that “I don’t know how to invest in the stock market because I use mutual funds” 😉 . Even if mutual funds are for wimps, those wimps often get the last laugh all the way to the bank.

After ruminating over my previous actions, it is clear that certain simple strategies yielded me good results, while others were just random shots in the dark that eventually cost me a bunch of money. What I learned is that a high net worth is not the product of a sprint but rather of winning the investment marathon with patience, savings discipline and a slow and steady approach to investing.

Copyright © 2008 The Digerati Life. All Rights Reserved.

{ 15 comments… read them below or add one }

Michael Jackson, eh? At least you got out before you’d lost the whole $12k.

Today I was talking with a patron about investing. He was checking out The Lazy Person’s Guide to Investing, which outlines some really nice indexes and promotes automation. He was more interested in real estate on the whole… But given the amount of time and effort needed to manage real estate vs. investing in indexes, I’m going with the latter.

I just love that final graphic…it is a wonderful visual for compound interest! Being the over-educated pizza delivery driver I am, I could rattle off the forumla for figuring compound interest but I think I like the graph better. My teenage son was asking me about it just the other night. Is it your visual? 🙂 As for the idea mutual and index funds “are for wimps” I say BAH! KISS principle is looking very nice in this current market…

It is really what is going to be comfortable for you and your risk tolerance. To many people at a young age are too conservative as well.

Risk=Reward, but Bad Risk=No Money…Gotta walk that line

Compounding growth is magic! Once the train gathers speed, it packs a powerful punch. And diversifying is critical. Many people I know didn’t learn the lesson you did – they played the market by placing all bets on one favorite stock or sector, watched their initial investment vanish, then swore off equity investing forever-more. Too bad they didn’t learn to diversify and ride the bumps instead, as you did.

Great illustration of these important investing concepts. I’m working on a relevant article and will link to your post here to serve as an example.

what i thought was missing from the story is more talk about the company’s fundamentals, which should have been the basis for your investment, not the media blitz by the company or the “hot stock” tip from various magazines.

Given that the stock was trading at an all time high, did the fundamentals justify it? Could paying huge sums of money to one “star” actually be recovered in market share or sales? despite higher stock price, were they continuing to gain market share? Were they maintaining their business model? much of what you wrote seemed to end up being emotional, which led to you becoming emotionally attached to the stock. When you start having an emotional investment in a stock or fund or money, it will invariably cloud your judgment, where you can convince yourself of anything rather than what is actually happening.

This is similar to a gambler who doesn’t know when to fold and walk away. you stop actually looking at the odds and the company’s fundamentals to justify your opinions.

the situation would have been no different if it had been a losing mutual fund. There is some risk mitigated in funds because of the diversification of assets within the fund, but you could have just as easily lost money if you continued to be emotionally involved in the fund rather than continuing to appraise the fund’s fundamentals.

the real lesson is to diversify as well as know what you are investing in, and not base your investing choices on what magazines recommend or the latest hype.

Compound interest is truly a wonderful thing. When I was 19 I realized that anybody, with any profession, can become a millionaire. By simply setting aside a portion on ones income (10-15%) and investing it into funds or stock indexes you can be a millionaire at retirement. It helps of course if you start early.

My first attempts to invest in individual stocks were also disastrous.

I am a lot more careful now, and also have some investments in mutual funds. (not index funds, though).

Our country has had more than its fair share of seriously ne’re do well fund managers who have brought $1 funds to 20 cents. So even mutual funds have their risks.

You say you track indexes, but which indexes? And isn’t index selection similar to stock selection although more diversified?

You can always be more diversified. Investing in the S&P500 isn’t enough. There’s are European stocks, emerging markets, commodities, alternative energy, and so forth.

Norak,

I’d like to address your question about what indexes I am talking about here. Thanks for a great question. I do have a follow up post to this one (which I still need to publish) that discusses in detail what kind of asset allocation to set up and indexes to be invested in, especially if you’re a first time investor. The reality is that every asset class that really matters to your portfolio is already represented by some sort of index. So the indexes out there already do cover diversification for you, no matter what asset class you can think of (e.g. international/foreign equity, bonds, commodities, and real estate).

Index selection is not like stock selection because an index is an index. What is there to select? The biggest decision you’d have to make is how comfortable you are with the type of indexes you’d like to have represented in your portfolio and what percentage of each asset do you want found in your portfolio.

That is, what is your risk profile? Anyway, it’s fairly simple when you stick to the basics. The selection and the monitoring of a stock takes so much more time than if you just stayed with indexes. For the returns and the effort, indexes really cannot be beat.

This is a great post and we’ve cited it in our Sunday Review Favorites. Keep up the great blogging!

Cheers,

FIRE Finance

The key is finding your comfort zone and how to be successful within it. it looks like you are there!

Best Wishes,

D4L

This blog post has been included in the “Carnival of Money Stories #51” at Life Lessons of a Military Wife. Hope you will drop by and read some of the many other wonderful entries received this week!

That is what it is about, finding something that works for you and keep at it. Good story.

I wonder what’s happened to your investments now? Are you still dollar-cost-averaging in this depressed market through your mutual funds?

@Zmeister,

Well yes I am actually! I have performed an asset allocation evaluation and determined that we need to shift several percentage points into equities. I am now dollar cost averaging in order to rebalance our portfolio according to our asset allocation of 60% equities and 40% stocks and bonds. So it’s all automatic.

This is a great market for long term investors right now. Watch it recover in a few years’ time.

By the way, I’ll be giving an update on our portfolio soon. So watch out for that post! 🙂