There’s a cost to paying only the minimum on your credit cards. To eliminate debt quickly, lower the interest you pay by doing a balance transfer and paying more than the minimum on your card bill each month!

The Cost Of Credit Card Debt

Paying off your credit card debt completely is one of the biggest financial accomplishments you can experience in your lifetime, especially if you’ve been living with (drowning in?) debt for a long time. It hasn’t personally happened to me, but I do know a few people who’ve been battling this type of debt for a very long time now, and who’ve been experiencing a lot of frustration with the process.

When you read about how people have paid off their balances, you’ll see how emotional they’ve been about their journey, and if you put things in perspective, you’ll see why this is such a huge accomplishment. Well here’s a success story in this vein: Tricia from Blogging Away Debt was able to retire her credit card debt load of over $37,000 in a little over 3 years. That is an awesome feat, especially how she was able to commit to this goal even while our entire economy remains in the grip of a world-wide financial crisis. It’s great to see how it’s possible to stick to a savings and debt payment schedule regardless of what else can be going on around you. And it shows that by making it a top priority, you can certainly eliminate debt by relying on your own steam, without necessarily having to resort to debt counseling or consolidation programs, loan modification, or even bankruptcy!

How The Costs of Credit Card Minimum Payments Add Up

One way to drive the point home about card debt is to demonstrate the consequences of growing debt. What happens to a hefty debt of 5 figures that is left unattended, ignored or mismanaged? We’ve been told time and again how such a debt is dangerous because it can very easily swell and get out of control, so much so that reining it back in becomes increasingly difficult. Just how difficult? Let’s see through this example!

As an example, let’s take the debt load of $37,000 and see how much it would cost someone to continue paying the minimum just to get by. If this debt were left to grow or if you decide to keep things status quo without a debt elimination plan, the results of this neglect won’t be pretty.

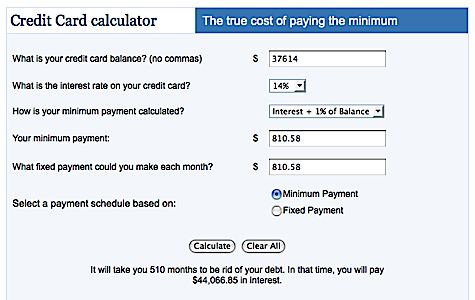

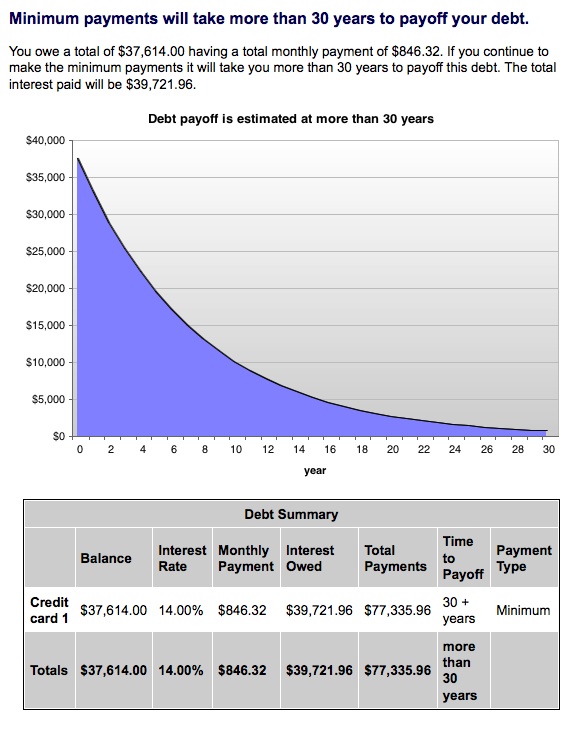

This may be simplifying things a bit, but I hope you get the gist. To find out the cost of credit card debt, I applied this debt example against a couple of debt payment calculators. I plugged in the average annual percentage rate for credit cards these days (14%) as well as a few default values. You may get a variety of results depending on your APR, but with a balance of $37,000 or so, you’ll probably have to pay a minimum of between $500 to $900 a month. Ultimately, results show that even if you keep to a minimum payment schedule, you could take several decades (30 to 40 years) to get rid of your debt. The interest you pay can end up being more than twice your original debt!

Case #1: Using the Bankrate minimum payment calculator. By paying only the minimum, a $37,000 debt can take you 42 years to retire.

Case #2: Using the Dinkytown debt pay off calculator.

The numbers may be different, depending on your circumstances, but the message is clear. That by doing nothing more than putting down just the minimum towards your debts, you won’t be retiring your loans anytime soon, thereby costing you more in interest over time. Credit card debt is no doubt one of the most expensive forms of debt available out there, especially if your rate is skyhigh (which is typically the case).

When Is Credit Card Debt Elimination Not A Priority?

But here’s something I also find highly interesting. Given the conventional wisdom that we should retire our debt quickly because it costs a lot to maintain this debt, we hear that Suze Orman, financial guru extraordinaire, is going against the grain to give us different advice. She suggests a different approach to handling credit card debt as we navigate through a different financial climate where credit is no longer as easily available as it used to be. With a poor economy and job loss so rampant these days, people with no savings are much more financially vulnerable during a time when credit is tight. So Suze encourages those without savings to prioritize on building their emergency fund first before working on debt payments. Her take? Pay ONLY the minimum until you’ve got your emergency fund (of at least eight months’ worth of expenses) squared away. For those with savings, then prioritize on paying down your debt as usual.

I like Suze’s arguments, although when I see a situation that involves hedging risk, I prefer to spread my bets a little. My personal approach would be to take my discretionary income and apply 50% towards building my savings and 50% towards paying down debt as fast as possible. Or how about paying down debt aggressively but leaving enough of a balance to preserve your access to credit? This way, you’re building savings while making sure your credit card debt doesn’t spiral out of control to end up costing you heavily.

Do you have any strategies for dealing with your credit card debt? All the various scenarios aside, and given all these facts and figures, I am sure that success stories like that of Tricia’s will only serve to inspire so many of us still working on chipping away at our debt balances. The one thing about paying off debt is that it comes with a psychological boost and an emotional high that’s hard to match.

Copyright © 2009 The Digerati Life. All Rights Reserved.

{ 16 comments… read them below or add one }

Credit card debt can easily get out of control. It takes self-discipline to use them discreetly and not let them get out of hand. We are an immediate fulfillment society.

Super post with super strong arguments. Thankfully most people are smart enough to know making minimum payments is a bad idea, they just aren’t smart enough to do anything about it. Ahhh the American way.

I think that when it comes to credit cards one should pay off the complete balance that one has spent during the month but with a lot of people they just can’t manage that and only just get by with the minimum payment.

I like the option in the calculator about the fixed payment. I have paid off most of my credit card debt from a high balance of $34,500 (now $5800), but I did it using a fixed payment of about $1000-1100 each month. I could have afforded to pay much more, but I didn’t want it to get in the way of my lifestyle. I would have regretted living life for nearly two years with little discretionary income, so I found a balance that allowed me to pay more than the minimum and still have enough to do the things I want. I have not accrued anymore debt, and I live fairly comfortably.

I don’t think people realize how much the interest builds up. People focus to much on the short term to realize how it can hurt them down the line. People need to be more educated because minimum payments are not good, people need to understand that and need to try to pay off as much as they can each month if not in full.

Minimum payout really makes my headache every month. They tell me to pay the min that to me, is already really high. So, the best part is to try to pay more than the min. Anyway, thanks for sharing that calculator: I really need it.

Paying off just the minimum is a death trap as the graphs above demonstrate. Do not buy what you can not pay for in cash. A simple statement to live buy, with the exceptions of real estate being something you should buy on credit, if you do not have cash for it.

Paying of a large annoying credit card debt is a great feeling b/c it gives you the financial flexibility to put that money elsewhere. I paid off my CC’s 6 months ago and I felt amazing…. that is… until I racked up a small amount over the last few months. Back to square one.

Credit cards can get out of hand so easily, and this illustration of the real cost of incurring debt is rather sobering. Thank you for some sound advise on how to mange the process of paying these burden off. Good Luck!

Thanks for providing the calculators. I blogged about this topic recently on bargainbabe.com and I found it useful to not only too at a calculator that shows the true cost of just paying the minimum but one that shows you how much more you could make if you invested in the money in an IRA: http://www.dinkytown.net/java/RothIRA.html

Hi

I think the potential problem with paying off your credit card rather than establishing an emergency fund is that your credit limit might be reduced. This has certainly happened to me in the past.

However I like your balanced approach to both points of view. Financial advice that comes “one-size fits all” is always dangerous. Take the example of someone in a very secure job (not sure I can think of one, but they probably exist!) with all their health insurance etc. sorted out. Is there any point them making the establishment of an emergency fund of 8 months expenses a priority over debt repayment? I think not.

Frontline had a great series on credit cards that you can watch on the PBS website. Highly recommended. It is from 2004 but if you look at what is happening today, and the legislation being proposed, it allows you to see what some were saying was going ot happen back in 2004. You can watch it online even. Link below:

http://www.pbs.org/wgbh/pages/frontline/

I forget who said it, maybe Dan Ariely, but minimum payment amounts act like a cognitive anchor. When you see that your minimum payment is only $50, you don’t think to pay the whole thing off… you think that you should pay $50. If you were going to pay more, you’d pay closer to $50 than to $100. In this way, minimum payments HELP the credit card companies because it unconsciously influences you into paying less!

It becomes so easy for us to use a credit card and end up in a large balance. And when it comes to paying it. It becomes difficult for us to pay. That’s when we end up in a huge debt.

Once in debt it is difficult to see any way out of it as knowing how to do so is not something that everyone knows the best way to go about doing.

I think people forget how much interest they are actually accumulating in debt.

I have Fixed Rate at 3.99%. The credit card company increase from 2% to 5% the capital. I called them and gave me the following options: First, Payment the increased amount of payment (my case from $210 to $498)……… or change my fixed rate to 7.99% to lower to 2% the capital. IS IT RIGHT?……….