I use a debt consolidation calculator to illustrate how much you can save with the right kind of personal loan.

Today, I’ll cover some ideas on how to become debt free faster. If you’re someone with a strong credit rating but with credit card debt and various loans to your name, you may be able to make bigger dents on your debt reduction efforts by opting for a debt consolidation loan.

Before I familiarized myself with the wonderful world of debt management, I never thought that you could do much once you got yourself stuck with credit card debt, or any loan or mortgage. But there are clever ways to deal with your debt if you’ve got fairly good credit. For instance, if interest rates go down, it’s always worth checking if refinancing your mortgage is worth pursuing. And what about all those personal loans, installment debt, revolving debt and credit card debt that you may be carrying? Well, if you’re money savvy, you can pay much less for your loans over time. While this is not necessarily news for a lot of debtors, it’s surprising that not more people are more strategic about working on a debt reduction plan that can expedite their payoff schedule.

As I mentioned earlier, you can stand to save a substantial amount of money when you have good credit. Having good credit is the basis for cutting down on the costs of borrowing. It’ll be easier for you to qualify for loans with the best terms if you sport a high credit score. And if your loan terms aren’t so good now, you can potentially improve your situation by applying for a debt consolidation loan that could very well be much cheaper than the combined amount you pay for all your disparate loans.

Use A Debt Consolidation Calculator, See How To Erase Debt Faster

So I mentioned debt consolidation loans earlier. This may prove helpful to you if you’ve got healthy credit, mainly because you can roll your loans over into one cheaper loan. You can be creative about this and it may just work! There are certain lenders that offer pretty good financing for smaller loans. For instance, why not compare your current rates and how much you’re paying on your existing debt against personal loan interest rates from a reputable peer to peer lender?

So how much money can you actually save with a better loan? How about I try to illustrate this point with some concrete examples: I went ahead and looked up some numbers, thanks to a debt consolidation calculator and some sample notes from Lending Club’s peer to peer lending network. Note that Lending Club is a company that offers personal loans through a different channel than that provided by banks and traditional institutions. Also, since rates are subject to change, exact figures may have changed over time (your results should actually improve in a low interest rate environment).

Case #1: Get A Lending Club Loan with A Low Risk Loan

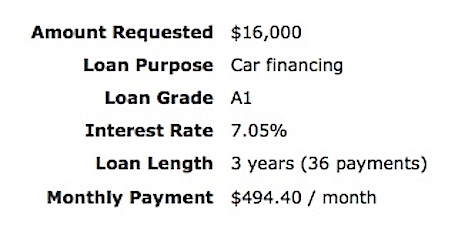

Suppose you want to finance the purchase of a car at $16,000. Some people will take out some auto financing to cover this purchase. But as an example, let’s say you decide to fund the purchase with the following loans:

- $5,000 advanced from Credit Card #1 at 15.90% APR (monthly payment is $176).

- $2,000 from Credit Card #2 at 19.00% APR (monthly payment is $73).

- $9,000 through an auto loan (monthly payment is $430) with a 24 month term.

- Total payment per month: $679

Now what if you took out a Lending Club loan in place of this existing debt? If you’ve got outstanding credit, you’re a very low credit risk and your loan will be considered high quality with a grade of A1. Here’s what your Lending Club personal loan would look like if you applied and got accepted into this peer to peer lending network:

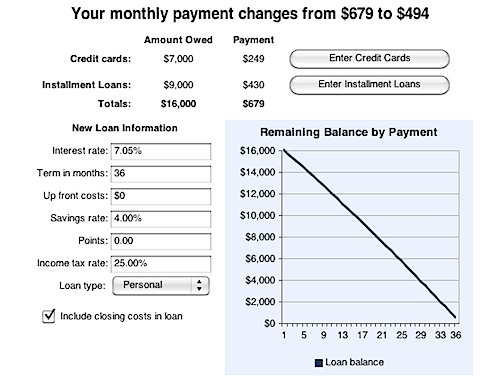

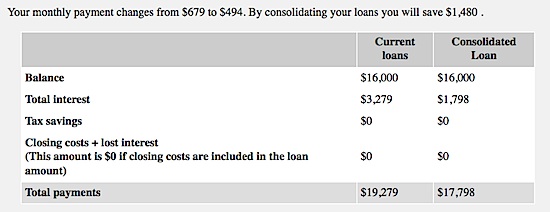

So if you use this loan to cover your car purchase instead, the debt consolidation calculator shows you these differences:

You’d be paying $494 a month rather than $679 a month. The interest rate at 7.05% assumes that your loan grade (measuring your risk as a borrower) is the best, at A1. In reality, this new loan will save you around $1,480. It’s money you can invest or apply to your loan in order to retire it even more quickly.

Case #2: Lending Club Loan With A High Risk Loan

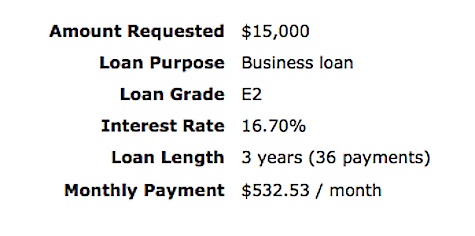

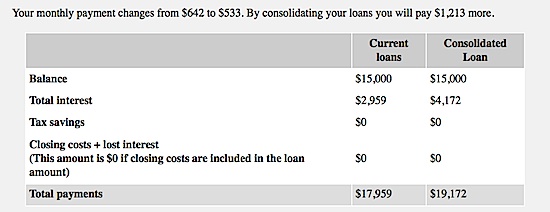

Now what if you’re a greater credit risk? Supposing you want to borrow money to start a business. You borrow $6,000 from your credit cards (with a monthly payment of $212) and you get $9,000 through a business loan (with a monthly payment of $430). You pay a total of $642 per month on this $15,000 startup loan.

Later on, you decide to consolidate your debt into a Lending Club loan because you qualified as a borrower. However, your loan is deemed a moderate to high risk and is given a loan grade of E2, with a higher interest rate of 16.70%. Again, the term is for 3 years.

So how much do you save? Unfortunately, here’s the rub: because of your higher interest rate of 16.70%, you’ll end up paying an additional $1,213 over the life of the new loan, even as your monthly payment shrinks from $642 to $533.

Depending on your requirements and needs, you’ll have to determine if a debt consolidation loan will work for you. In many cases, it may be the ticket to savings, but as you can see, it’s not always the case. If your payment terms are not great, you could pay more in interest over time. Sure, you’ll pay less on a monthly basis, and this may be what you’re after, but be aware of the overall costs you could end up facing if you go down this route.

Created December 28, 2009. Updated November 30, 2012. Copyright © 2012 The Digerati Life. All Rights Reserved.

{ 9 comments… read them below or add one }

Hrm, if 7.05% is the best lending club can offer with an A1 (I assume the best credit rating?) score, most people can do better. I was offered a 6.75% by my credit union, and 5.99% by my toyota dealer, with a 787 credit rating.

Katharine,

That’s actually good to know! Lending Club’s rates are “universal” so to speak, so if you shop around and find something better in your neck of the woods, that’s great! I think the message here is loud and clear though, that it pays to shop around. I would clearly expect variations in rates across the board so do check around. If consumers shopped as carefully for the best financial deals (or looked for the best financial products) as they did their groceries or other goodies, then they’d be way ahead with their finances. I believe that the best savings you can get aren’t from the savings offered by stores, but rather from savings you get through smart moves with your money (e.g. picking up the best terms in loans, choosing the right broker or mutual fund company with the cheapest fees, etc).

What often happens with products such as mortgages, loans, insurance and so forth: people ask family members or friends to recommend the best “agent” for them (or blindly take whatever available financing is offered by an establishment without cross checking) and consumers go with the first thing they come across. What a lot of people don’t realize is that by window shopping at retail stores all day they’ll save hundreds (maybe), but by spending the same amount of time doing the research on big ticket items, they’ll save thousands over time.

Debt consolidation calculators are extremely helpful, as you pay off debts. Many people use these just once when they make their payment plan, but it’s important to remember that life situations and standards of living change and when they do it’s important to use these kinds of calculators to reestablish payment plans.

I see the value of debt consolidation loans but I think your examples are somewhat shaky. I was able to get about 6.9% on a car loan which is already lower than the debt consolidation loan. Whoever is paying a car loan with a credit card is just insane. I think these consolidation loans are best when paying off credit card debt (as in your examples) but it’s more likely that debt was accrued through spending up to a credit limit on random items than on large purchases.

@Edwin,

Good points. If you’re paying off a car purchase with a credit card, then you’re not thinking things through…. Anyway, yes, you can always find better rates for other types of loans, such as car loans and mortgages. You can’t really compare the 2 because these are collateralized loans (if you miss a payment, the auto financing company can take your car back, for instance). You’re likely to get a 5.7% interest on your car, as well as a 5.25% on a mortgage, for instance. The example was for purposes of illustration, but the car loan is probably not a good example — perhaps a loan for a given event, say travel or a wedding may be better examples.

Credit union loans are a more comparable option to Lending Club loans (when it comes to rates) if you’re talking about lines of credits or personal loans (without collateral). But be aware that in most cases, you have to have money in your savings account and maintain a minimum to qualify… which means they are lending you your own money 😉

You bring up a good point, the loans aren’t backed by anything. Meaning although you may be paying a higher rate, you own your car no matter what happens and they don’t get to hold your title until repayment.

Great article… this last recession we had clearly shows that people really lived outside there means. Last week on CNN they stated that the average American is in $70,000 worth of credit card debt. A HUGE sum of debt to be under. I tried finding the source but couldn’t locate it, if anyone finds it please post it.

Thank you for submitting your article to my weekly Financial Independence Compilation.

Hey SVB,

Good posting. I am curious as to what your thoughts might be on personal loans other than prosper. It has been a while since I looked into the issue…can you get favorable terms at a credit union?

James