Have you started to teach your children about money?

As a parent of school-aged kids, one thing I’ve wondered about was when and how to introduce the concept of money to my kids. Many parents start early, explaining the whole process of earning, saving and spending to their children as soon as they understand that their cool piggy banks aren’t just toys, but are also great financial tools. 🙂

I could tell, however, that the concept of money wasn’t something my kids could grasp early on, so I deferred the money lessons until recently. I think it’s time to let them know what all those coins and bills are all about.

Lots of you believe that the best way to teach your children about money is by giving them an allowance and by allowing the kids to learn through practice and application. My neighbor has a child in middle school who’s already fully aware about the concepts of saving and investing; he’s even bragging about how much he’s made on his Disney stock — and he’s only 10! Plus he’s extremely enterprising, often going door to door to sell his services to families (e.g. babysitting, petsitting, gardening, etc.). His parents sure did a great job of granting him an early financial education.

Your Kid’s Allowance: How Much To Give Your Child

I’d actually like to know how much of an allowance to give my kids. Apparently, the rule of thumb is to give a child $1 a week for each year of age. So a 6 year old is supposed to get $6 a week. To me, this seems like quite a lot (and for such a young age), or maybe I’m just out of touch? 😉 I got these results from this allowance calculator.

If you want more information about how to teach kids the value of money and how to manage it well, check out TheMint.org, an educational site that offers resources for grown ups and kids alike. For fun, I took a look at one of the studies they conducted, which was taken by 2,000 respondents. The study was on the subject of allowances, and provided these cool graphics:

|

|

|

|

Some of the findings in this study:

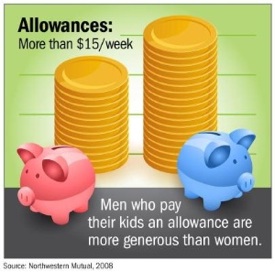

- Men are 3 times more likely to say “NO” to an allowance (compared to women).

- But those men who decide to give out allowances at all are actually more generous than women.

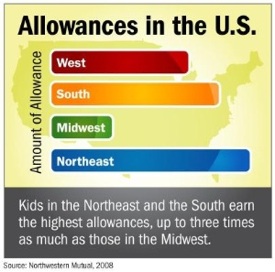

- Parents from the Midwest are cheapest about allowances. Those in the South and Northeast give three times more (for allowances) than their Midwestern counterparts.

- 70% of parents agree that a 10 year old should receive between $1 to $10 a week as an allowance.

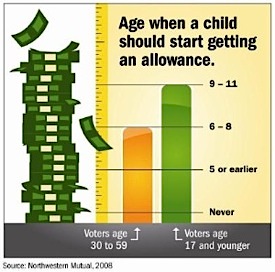

- 65% say that the best age for a child to begin receiving an allowance is between 6 and 11 years of age.

While I learned some really interesting things from this survey, I do still have more questions on this matter: should you pay your children to do chores? And should you reward them with money for other good behavior (such as getting good grades, not getting into trouble, etc.)? There seems to be some debate about this, but I’m of the mind to give a kid a flat allowance to help the child understand the basics of saving and spending; I’m also open to having him/her “earn” extra bucks for going “above and beyond”.

Now for some parents, “above and beyond” includes chores and good grades, while for others, such good actions won’t count toward rewards since this behavior is what they already expect from their child. And there are those families that have the “earn your own allowance” policy. Whichever way you go would depend on your parenting style. So what do you think? Please free to share your ideas with us!

Copyright © 2009 The Digerati Life. All Rights Reserved.

{ 23 comments… read them below or add one }

Jane 2.0 is 10 and gets her age. She is tight with her money, and has managed to save quite a bit from this allowance, birthday/holiday gifts, and recent money earned baby sitting/mother’s helping. We pay for her ‘needs’ but ‘wants’ come out of her money.

should you pay your children to do chores?

My kid is still very young, but he knows what he should do from coins he gets from my pocket 🙂 as I’ve written on my blog.

But I feel I’d not want him to just focus on money, other forms of rewards can also be alternated here. Maybe if he wants to spend more time with me, then I’ll get him to complete a set of chores first. and he gets to decide what we ant to do after that, like a trip to the cinema, park, etc.. you know, things like that..

The next round, offer cash..

I think people sometimes miss the boat with allowances. Sure it teaches kids how to work and earn, and this is a good concept. But it does not teach kids how to shop and necessarily save. How many times do you pay a child, and they run out and spend the entire amount. Do you know adults who do the same thing? I do. Now wonder where they got that habit?

Its good to teach kids how to earn AND how to save. How much you pay them is not the important thing in my view.

When I started getting allowance as a child I was SO excited to finally have my own money. Little did I know, the phrase, “Save your allowance.” would soon invade my life. My parents gave me an allowance once every two weeks (when they got paid) a dollar for each grade year that I was in (i.e. $5 for fifth grade). It wasn’t much, and I didn’t have much to spend. By the time I got to high school, I was desperate to start working and making more than my measly allowance. While I wasn’t given a lot of money to work with, I was taught to budget and plan for things that I really wanted (an $85 Princess Diana beanie baby) and skip the things that I didn’t really need. I don’t think that kids should be given too much allowance because this teaches them that it’s too easy to make a lot of money, and they take it for granted. Plus, it makes it harder for the parents to cut them off when it comes time for the real world to set in.

This is a very interesting post, regarding teaching kids about handling money.

For me, I have the opinion of starting from very young age, when your kids know what is money. It does not matter whether they are in pre-school and do not use money much, but at least you introduce the allowance money and some saving up mindset.

I don’t think it’s beneficial for a child to receive money for doing chores. It’s something they should be doing around the house anyway; will they expect to be paid for keeping their dorm room clean when they go off to college? What about a house or apartment?

That said, I do find it beneficial to pay children for work outside their normal chores; things that you as a parent need done for yourself, for example, rather than things the child should be doing anyway.

We have a system that has worked quite well for us. $1 for each year in school. My 3rd grader gets $3/week and my 8th grader gets $8/week. Works well and seems age appropriate.

I am down to one child to pay allowance to. She gets $15 a week allowance and $5 for school lunch. She always has the option to make and take her lunch. She is 15 and has a healthy savings account. She knows how to save her money and now has her sights on a car for senior year in HS. I do not know if she will make that goal.

Tradition in our family has been that when you work full time, during the summer, no allowance. She has spent 2 years as a CIT and plans to be a paid counselor next summer.

At 18 or graduation from HS no more allowance. This has been tough on my son 18 and a freshman at local community college. The market to get a position local big box even is not there right now. Hoping he will find seasonal work for Christmas.

These are great ideas! Haven’t started my kids (well only one qualifies really) yet on an allowance, so all your opinions are very helpful. I like Cathy’s idea on paying them according to school grade, rather than age ($3 a week for a 3rd grader seems to make more sense rather than $8 a week based on a 3rd grader’s age).

@Karen, looks like you’re home rules are doing wonders! Clearly, a family’s influence goes a long way in establishing a child’s financial mindset.

@John Gerber, I gather the allowance should not be attached to the chores and other expected tasks. Or are you suggesting that we don’t give a child an allowance at all — just have them earn it for extra work they do? I guess I’d think of an allowance as just a general stipend you get per week (with nothing attached).

i don’t have kids and to say the truth i don’t think that i am close to getting any but let me put my two cents in (i am extremely opinionated). Concerning cash, the first thing that my kids will learn is the golden rule; “he who has the gold makes the rules” so it follows simple logic that the more gold you possess the greater your power over almost everyone and everything around and that means that they can call the shots…..like their daddy 🙂 That’s my piece!

I kind of agree with 1$ for every year formula. but another interesting question is what age do you really start giving allowances? any thoughts?

My boys are grown. I can’t say they had allowance. There was chores we paid them to do. They where chores we didn’t pay for.

We where real poor when the boys where at home. Part of the time we drew food stamps .

But we always some how figure to find the extra cash for our boys never to be left out. As I recall when they left town and usual they stop at McDonald they had $5.00 or $7.00 to go and get bite to eat like the rest of the kids.

We taught our kids a meaning of buck. Now there own and putting there way though college.

Coffee is on.

We give our children $.25 per day IF they fulfill their responsibilities around the house in a timely manner. Which is really just one chore each. Allowance is only tied to chores insofar as the children are not a drain on how our household operates. Our children are all under the age of 10 and still learning that they have responsibilities and we depend upon each other for our lives to run smoothly. If they earn a quarter every day for a week, that’s $1.75. My husband and I only give ourselves $5 a week each for our own allowance, so I don’t consider theirs to be too shabby.

I enjoyed the post… Some may find this to be a bit much, but I’ve got an allowance plan I’m still working on with my kiddo.

I have a 10 year old. She does not get an allowance. Instead I put $10 per pay period ($20/mo)directly into her savings account to get her some savings started. I plan to let her manage these funds as she gets more mature. If she wants to earn some money, I will pay her to wash the car. Since it costs $10 at the car wash, I will pay her $10 if she wants to do it instead and does a decent job. We also have a list of “extra” chores that she can do for $1 per chore. These are things like sweeping the house – I do not pay for her cleaning her room, picking up after herself, or any other expected chores, only “extra” stuff and we have a list of what qualifies. At this point she is not too motivated. . . I think as she hits middle school next year and wants to do things with friends she may be more interested in working to earn and have some pocket money.

We pay our kids (7 and 11) an allowance on a monthly basis and it had been $30 until a few months ago. In honor of the recession, we gave them a STIFF pay cut and stripped it down to $10 per month. You can imagine the horror and shock when we made the announcement, but since then, we’ve found that they adjust quite well. Instead of buying several packs of trading cards, they buy one. Instead of blowing it all right away, they take a little more time making decisions.

It’s been an interesting experiment as they are essentially doing what most consumers are doing – cutting back. We’ll probably increase their allowances again sometime in the future, but we thought it important to let them participate in the recession and teach them that even if you do a good job, there are forces at work that can still sidetrack you.

BTW, of the $30 they were ‘paid’, we kept 30% or $9 each month back for savings. They asked to have the money since they were experiencing an ’emergency’, but we explained this didn’t qualify. It’s difficult to teach all of the lessons they’ll need when they become adults, and some lessons will have to be learned the hard way. However, feeling the pinch of the recession has been fun. For the record, they are no more or less happy as a result of their pay cut.

My children are now 19 – away at university and 14, so we are now down to one allowance. When the oldest was 4 we moved to the dollar a year based on age with one caveat added about age 6. We explained that the $6 had three purposes and here is how he was expected to allocate it. One third was for university which he was interested in so that he could study dinosaurs, one third was for charity which has mostly been our local church and the final third he could spend on anything he wanted, no questions asked. At age 6 that was mostly model trains, and as he aged it changed to Lego and then even games for his various electronic devices.

We saw it as a way to build character and goal setting. We knew when he wanted to spend $100 on some electronic device that it was really important to him because of how long he saved to get that money. Now that he is in second year university, he seems to have good financial restraint.

Our daughter was a little different. The money was the same, but the challenges were different. When she was about 11 and Christmas rolled around she was devastated that she has blown almost all of her money and could only buy very small presents for her brother and mom and dad. We talked about it and I suggested saving a dollar a week out of her fun money. Next Christmas she was so proud to have a huge $75 for Christmas. Not only had she done the dollar a week, she had topped it up with some of her birthday money.

Money and finances have always been more of a struggle for her, which is a reflection of their ability to plan for the longer term. He has no problem; she has lots of challenges. In the end the money amount is less important than the opportunities that it allows affords. Better to blow $40 when you are young that buy that silly sports car when you are old and for the first time have buyer’s regret.

This past summer we started a paycheck plan with our 13 and 15 year old sons. First, we took them to our local credit union to open up a savings accounts. I made a list of household chores that they had to complete in a time frame of 8 am to 12 pm. each weekday. After 12 pm they could enjoy their free time. Every Friday we wrote each son a check for 30 dollars. They were responsible for riding their bikes to the bank to the cash their checks, taking out the cash they needed for that week, and depositing the rest for savings. If they needed more cash throughout the week, they could go to the bank and make a withdrawal.

Once school started, they were not home during the day to complete a regular work load. Instead of decreasing their paycheck amount, we kept it at 30 dollars and made them responsible for depositing 10 dollars a week into their school lunch accounts. They are still responsible for regular chores, but their chore workload has decreased due to homework but they now have the opportunity to earn more money by completing extra chores. We will be encouraging our oldest son to pick up a summer job next year, but we will still pay an allowance. Currently, they are each managing their accounts responsibly and saving money for personal goals.

The biggest benefit, has been for my husband and I. We no longer have to “shell out” cash last minute and our kids have not had to ask us for any money.

Just for being in our family the children get $1 per year of age (after reaching 5 years old) each month. It gets divided into fourths and divvied out weekly. But there are a few catches.

1. Necessities come from Mom and Dad. Splurges come from your allowance.

2. 20% is put in a savings account. 10% is donated and 70% is for whatever the child decides. We help the child learn about saving up their 70% for the toys they want.

3. If you don’t do your chores by a given deadline, they go up to the lowest bidder who has already finished all his/her chores. For example, if child A doesn’t want to wash the dishes, children B, C and D offer their bids to do it. A then has to pay the lowest bidder their asking price (it’s capped according to the chore).

We first tried giving them all the money up front at the beginning of the month. All the excitement fizzled out by the end of the first week. We don’t want to give them too much because learning to save for more immediate pleasures and developing the behavior to fight off impulse purchases work best on smaller allowances. That’s why we divided their age by fourths, then hand out that amount each week (they make a little more money that way, but I don’t care as long as they learn good lessons with it).

They can occasionally get paid bonuses for chores that Mom or Dad forego, provided they have already done their chores. This further motivates them to be done so they have that availability.

Using this method they learn about saving, spending, earning, preparedness, frugality and charity. So far it’s working well. We adapted the idea from Jim Fay’s Love and Logic.

Our children must EARN their allowance, no freebies!! As a single parent that was *less* than good with money throughout my youth, teaching children about money is CRUCIAL, in my mind. I’m not going to blame parents, schools, etc, but quite simply, I clearly “didn’t get it”, and I am still paying for those mistakes a decade later! And quite frankly, I hate the position I got myself in, everytime I pay off my past debts… I could have used my time/money sooooo much better.

You should also teach them about how to best spend the money. Of course, you can’t really teach them how to invest. But they can invest in their own little way. For example, they can buy books with their allowance instead of candies. But as soon as they can understand more complex things, you should teach them how to invest properly.

I’m 15 and I get $15 a month. I get payed weekly though with $3.75. My family goes by the age and that price a month, so my little 7 year brother gets $7 a month, so he gets $1.75 a week. However, we don’t get paid if we don’t do our weekly chores.

My 13 years old sister and I trade off every other week. One week one of us will clear the dish washer and stack the dish washer after dinner. Then the next week the other will do it. Then every week we have to vacuum our bedrooms which keeps them clean.

My 10 year old sister has to clean the dog run every week and vacuum her bedroom.

My 7 year old brother feeds our dog and the fish every morning. Then he helps my dad clean the fish tank when it is needed. He also needs to vacuum his bedroom once a week.

On top of all this there is a chore chart with extra chores we can do to earn extra money when we need it. We need a good reason to earn the money such as saving up to buy something or going to the movies with a friend in a few days. You can’t just do them to gain extra money. On it are things such as cleaning the bird cage for a $1 to mowing the lawn for $10.

I think this system is fair because with my $15 a month I have to budget it, but I can still go to the movies 2 times that month.

This system works for us.

Sunbird Opportunity Funds has neat college fund that acts like an allowance. Parents may join for a one-time fee of $2,500, and start receiving monthly payouts of $105 by check or direct deposit. Parents may choose to pay their children for good behavior, or keep all or some of the money in the savings account. Equity accrues in the member’s account in monthly matching payments, so that after 6 years of membership, monthly payouts rise to $420 per month. By college age, kids may have many thousands saved for school!