The cornerstone for many a long term investor’s approach to investing is market diversification, asset allocation and risk management. We cover these topics quite often over here. But I thought it would be nice to revisit the basics, using the fancy term that academics use as the impetus for a solid investment strategy: Modern Portfolio Theory. So I’ve invited a guest blogger to discuss this matter a little bit. Tim Parker from Elementary Finance shares his thoughts on MPT today:

Modern Portfolio Theory (MPT): Manage Risk With Diversification

Have you ever heard of Modern Portfolio Theory? Even if you haven’t heard of it, you almost certainly use its rules as part of how you manage your investments, so let’s take a look at what it is. The shortest answer is that Modern Portfolio Theory is learning how to manage risk. Not just looking at the risk in a stock, but what kind of risk that stock adds to your entire portfolio.

1. Let’s discuss diversification.

Modern Portfolio Theory has its roots in an article published in 1952 entitled “Portfolio Selection” (by Harry Markowitz). The premise here is that it’s not a good idea to invest in only one stock because if it goes down in value, it takes your entire portfolio with it. Instead, you should invest in a series of investment instruments so that your entire portfolio isn’t exposed to too much specific risk. (Specific risk is that which comes with a certain individual stock rather than what you’d find in a larger economy.)

Does this sound familiar? Diversification is one of the fundamental ideas behind developing an investment portfolio and this concept comes from Modern Portfolio Theory.

2. What about hedging to manage risk?

You may recognize this part of the theory as well: in order to minimize risk to your investment portfolio you should have some safe haven investments (such as liquid online bank accounts) to insure your portfolio against too much loss. For example, you could invest in gold so that when the stock market stumbles, your portfolio doesn’t suffer the full brunt of that fall if gold rises or holds its value. This is called hedging. The idea here is to pick asset classes that are not strongly correlated to each other such that market movements by these financial assets are less volatile (or made smoother) over time. Check out this article about the optimal foreign investment allocation that can help hedge your portfolio against significant risk.

So to sum things up, Modern Portfolio Theory states that good investing isn’t just about picking stocks but about picking the right combination of stocks. Managing risk is the key.

Issues With Modern Portfolio Theory

While this theory is accepted in the investment world, there are some potential issues with it. First, in order to avoid risk, it is suggested that the investor gain true diversification by picking stocks that are unrelated to each other. Unfortunately, to do this on your own can be pretty tricky. Here’s why: if you listen to Jim Cramer, he says that 50% of a stock’s movement is based on the sector that it is in. If the sector moves down, so does the stock in many cases. If you have been an investor through a big move in the market, you know that when an index makes a large move, nearly all stocks move with it. As it is, there’s a lot of correlation in the U.S. market among the individual stocks that make up this universe. So how diversified can we really get?

Other critics ask the question, how many investments are needed for true diversification? Some mutual funds have dozens upon dozens. Some theories state that twenty stocks is enough, but how many stocks can a portfolio have before they overlap? That is the main problem with this theory. At best, you can diversify using indexing, mutual funds and ETFs, and buying into different asset classes for some representation; hopefully, this helps you achieve reasonable market returns. In my mind, just as long as I beat savings account rates, then I’m good to go (but with recent poor stock market returns, that hasn’t even been the case, unfortunately).

If you subscribe to Modern Portfolio Theory, you believe that the market can’t be beaten without taking above average risk, so in order to make money, you’ll need to focus on how your entire portfolio is doing, rather than having a single stock perspective. For those interested in a diagram that illustrates this theory, click here.

Copyright © 2009 The Digerati Life. All Rights Reserved.

{kind=link}

{ 16 comments… read them below or add one }

Isn’t it Warren Buffet that says that diversification is for lazy investors that don’t know what they are doing? Personally I’ve also handed my money over to “professionals” and paid a handsome fee only to see them lose just as much money as if I had invested in the index myself (actually more since I wouldn’t be paying the fee also). So questions is whether you really want to diversify and hope that someone else will take good care of your money or whether you would be better off actually learning how to invest and not only save the fees but also make sure that the one taking care of your money (aka YOU) actually cares about them.

“If you subscribe to Modern Portfolio Theory, you believe that the market can’t be beaten without taking above average risk”

I think that you may be confusing two concepts in the quote above: Portfolio Theory is different from Efficient Market Theory. Efficient market theory postulates that the value of a stock (and of the market in general) reflects all publicly available information about that stock. Which means that you are not going to be able to consistently beat the market over the long term, when taking into account such things are transaction costs, unless you have insider information (hence the ban on insider trading, btw).

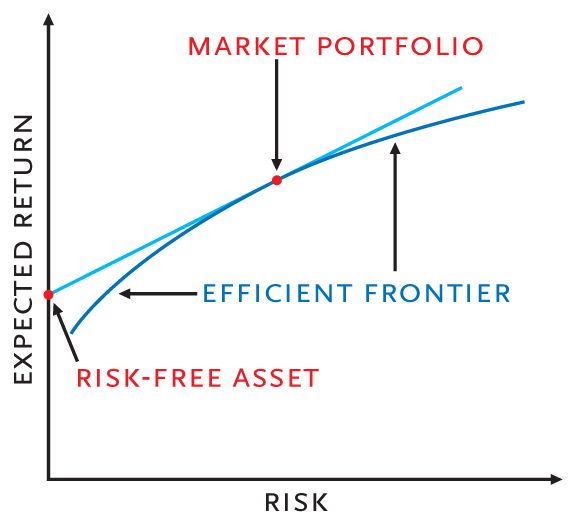

Portfolio Theory (and the diagram to which you point) is about how to select the mix of assets in your portfolio. Generally speaking, it is true to say that risk and return are positively correlated, i.e. riskier assets will tend to offer higher returns and vice versa. The chart you point to shows that you can take on as much risk or achieve any desired level of expected return by using only 2 assets: a risky asset (a single stock, for example) and a risk free asset (usually a treasury bond is the example used in this context).

The dot on the chart that is labeled market portfolio is equal to a mix of 100% risky assets (the said stock) and 0% risk free assets (i.e. treasury).

Good attempt at a tough subject.

Shadox,

Thanks for the clarifications. There’s definitely a lot of theory behind the stuff we take at face value when we invest. One of the goals I have (as well as that of many bloggers such as yourself, I’m sure!) is to try to simplify some of these ideas, and I agree that there’s a lot of tough material out there that sure could use some discussion and dissection.

I like using these types of articles as a way to learn more about the subject. I find the charts quite fascinating in a lot of these models, and look at the theories as a way to explain the reasons behind and importance of the investment strategies we end up embracing.

Very often the underlying concepts of a theory are taken as a given and so when the real debate on the theory should be on its assumptions — that never takes place. And then years afterwards you find that the whole damn thing was based on flawed assumptions. Like the whole deal of economists saying for a number of years that the customer is rational and all that till someone came along and reminded them that the customer is not rational, the customer is your wife.

If you buy gold when the market is down, chances are that gold would already be at quite a high price (like today) and so you will exit one over priced asset and then get into another.

It’s good to be aware of these theories and Tim makes a good effort of explaining this stuff, but, we need to be aware that for a long time in our history we thought that the world was flat. There is no reason why we couldn’t be wrong about EMH, MPT, TARP, PPIP, KFC? any of that stuff.

Ouch I’ve got a headache. As we have recently learned, sometimes its just a crap shoot no matter how much managing is going on.

That diagram was worth several Nobel prizes, so we might as well explain it properly.

The dark blue curve, the Efficient Frontier, represents all the possible portfolios of assets (stocks) that are efficient, meaning that there is no other portfolio that is both higher return and lower risk. There are, of course, an infinite number of other portfolios you could construct. They would be plotted on the chart as a great cloud under the frontier. The frontier is the edge of that cloud, the subset of portfolios that might make sense for an investor who, for example, desired the most return at a given level of risk or the lowest risk for a desired level of return.

However, if we add in the ability of the investor to either loan or borrow money at the risk-free rate, it turns out that there is only one portfolio of risky assets that is efficient. That’s the red dot in the center of the diagram labelled market portfolio. For any other desired level of risk or return the investor can do better than the efficient frontier by owning some of the market portfolio and either owning some risk-free bonds (when to the left of the market portfolio) or borrowing and taking on leverage (when on the right.)

And what is this magic single efficient portfolio? It is the capitalization weighted index of all publicly traded risky assets, commonly approximated by an index such as the S&P 500. Hence the name market portfolio. I.e., it’s not “a risky asset” it’s all of them. Leave one out and you’ve given up some diversification and are sub-optimal.

Shadox is correct – there’s a difference between modern portfolio theory and the efficient market hypothesis, but there’s some overlap. Modern Portfolio Theory is largely based on an adherence to a belief in the efficient market hypothesis.

Changing gears, Joel Greenblatt has several very good discussions in his books about diversification. Having a portfolio of 20 stocks makes you only slightly more diversified than having a portfolio of 10. I don’t have the math in front of me, but he makes a very convincing case that many people are over-diversified on the recommendation of their financial advisors.

Good post.

Would watching a few specifics stocks carefully be better then diversification?

I think Modern Portfolio Theory is dangerous nonsense.

It used to be that you would see one or two articles a year saying this. Since the crash it has become one or two per week. Buffett recently said that the conventional investing advice (rooted in Modern Portfolio Theory) is “nutty.” That says it, in my assessment. Wharton recently had an article arguing that the economic crisis was caused by economic theories that ignore all of the most important influences on the questions being examined. That’s Modern Portfolio Theory.

Rob Arnott has said that we are in the early days of a “revolution” in our understanding of how stock investing works. It cannot come soon enough for me.

Rob

I think we all learned over the past year that efficient markets don’t exist. Is it possible that the “value” in the market was never lost, it just never existed? Yes, I hate hearing about the decline in the value of the market. It never existed.

On another note, anyone have any thoughts on munis right now. I still can’t really figure out when the treasury bubble will burst and muni rates will return to normal levels (below treasury levels).

This is why so many beginner investors do well with mutual funds. they provide instant one step diversification particularly index funds

I am really interested in learning about the stock market and from what I have read two good strategies are diverification and research. Hopefully by the end of 2010 I will have enough info to invest without loosing it all instantly.

Have you noticed how every time a crisis hits, there is a camp of people who like to talk about how it’s different this time? I’m not old enough to have gone through many economic downturns but I’ve seen this played out in more areas than just finance and it’s just as true. How often lately have I heard that buy and hold is dead? How will we know if buy and hold is dead? Not nearly enough time has gone by to “hold.” Let’s ask that question in 10 years after we have held. I bought GE at $10 and you can believe I’m buying and holding. It might get me in the end and some of you can tell me that you told me so but I’m pretty confident that I have GE at an amazing price and down the road, I’m going to feel pretty good about my buy and hold.

This is no different than other downturns. The only way it would be different is if we never recovered.

Genuine diversification is becoming increasingly more difficult to achieve. According to Bloomberg, “the Standard & Poor’s 500 Index, whose increase in the past three months was the steepest in seven decades, is rallying in tandem with benchmark measures for raw materials, developing- country equities and hedge funds. The so-called correlation coefficient that measures how closely markets rise and fall together has reached the highest levels ever.” The correlation between the S&P 500 and the Reuters/Jefferies CRB Index increased to 0.74 in June according to Bloomberg up from the previous high of 0.66. The correlations between the S&P 500 and crude oil and emerging markets are also at or near record highs.

Despite this data there are definitely asset classes in which investors can still get diversification benefits.

Research by Agcapita Partners, a Canadian agriculture private equity firm, shows that one of the beneficial investment qualities of farmland in North America is that is has a very low (slightly negative = -0.13) correlation to stock market returns. In general, this has meant that by adding NA farmland into a stock portfolio you improved diversification benefits. By way of example, when stock markets were falling globally in 2008, Canadian prairie farmland went up approximately 10% in value.

Efficient Market theory is clearly mostly wrong 😉 Asset prices swing back and forth between cheap and expensive. I think that Modern Portfolio Theory is actually more insidious and dangerous though because so much of finance takes it for granted without checking the base assumptions. If the assumptions underlying a theory are wrong or over-simplified then you would expect the theory to fail in real life. MPT was certainly a major step when it was first proposed in 1952, but it has some serious flaws based on broken assumptions:

Flaw 1) Average period returns for assets are used instead of compound returns. For high volatility assets the average (mean) return is substantially higher in value than the compound return you actually end up with a the end of the holding period. This means that MPT based portfolio optimizers called “Mean-Variance Optimizers” put too much weight into volatile assets.

Flaw 2) MPT equates standard deviation of returns with “risk”. Returns of +5%, +25%, +5%, +25% alternating would have a high standard deviation but most people wouldn’t consider it risky because there are no losses. Would you rather hold a portfolio that earns larger losses in order to achieve better standard deviation of *mean* returns? That is the trade MPT makes.

Flaw 3) MPT thinks that correlations during good times are important – but they aren’t at all! Nobody cares if assets are un-correlated during good times because this doesn’t keep everything from plunging during a crash.

This is getting long but hopefully useful for someone! Here is an example from some research I am working on. In the beginning of 2007 a MPT based mean-variance optimizer suggested this portfolio:

Total US Stock Market 48.1%

Foreign Stocks 32.2%

US Bonds 14.9%

Commodities 3.5%

REITs 1.3%

Here are the performance stats:

CAGR ’71-’06 11.4%

CAGR ’71-’08 9.7%

2008 loss -32.7%

A different optimizer that fixes the 3 broken assumptions underlying MPT would have suggested this portfolio for the beginning of 2007:

US Bonds 39.6%

Commodities 27.7%

REITs 19.1%

Foreign Stocks 6.8%

Total US Stock Market 6.7%

The performance through 2008 turned out better with the second approach:

CAGR ’71-’06 11.4%

CAGR ’71-’08 10.1%

2008 loss -22.5%

Reference: http://www.riskcog.com/mean_variance_comparison.jsp

@Matt MacClary

You raise some good points. I do think that using mean-variance optimisation to construct portfolios definitely is helpful, but the key is to understand it’s limitations, to use improved versions of the theory that tackle some of the issues that you raise, and, perhaps most importantly, to supplement this with other approaches that don’t use these assumptions. Like stress tests, Value at Risk and Monte-Carlo simulation.

On flaw #1: You’re absolutely right for most optimisers, but better ones use ‘multi-step’ optimisation to get around this problem.

On flaw #2: It’s true. That’s why we think it’s important to analyze risk from many angles and perspectives, over and above traditional ‘volatility’. For example, looking at historical worst-case losses, scenario analyses and stress tests are robust ways to put potential portfolios through the gauntlet to see how they performed in the past, and are likely to perform in the future.

On flaw #3: What I’d add is that standard mean-variance optimisations assume that correlations (and volatility) are constant over time, when in actual fact we know that they both spike in times of trouble. Good software should allow you to measure how ‘unstable’ asset correlations and volatilities are, and then incorporate this information when building and stress testing potential portfolios.

Ultimately, all ‘models’ have their flaws, and financial models are no different. The trick is to understand their limitations, and use a number of different models / techniques and cross-check their results. That’s about as close to an all-weather portfolio as you’re likely to get – one that should see you through thick and thin, for the long run.