A while back, I covered the world of social lending, when I was relatively new to the whole peer to peer lending premise. Now that I’ve become much more familiar with it, and have had some time to see how things operate in this field, I’ve decided to review how the industry’s been doing so far.

Image from people2capital.com

Image from people2capital.com

If you’re not familiar with the peer to peer lending concept, it’s a way to lend and borrow money through an online network. This lending platform basically matches borrowers and lenders such that borrowers get their loans funded at usually much cheaper rates (vs traditional lenders such as banks and credit card companies) while lenders (also called investors) earn a rate of return on the money they lend with the potential to beat investment returns from other avenues.

List of Peer To Peer Lending Networks

Here’s a quick introduction of who’s who in the peer to peer lending space:

1. Lending Club

The buzz on this lending network has been pretty positive: they’ve recently passed some serious milestones for issued loans. I know a few bloggers who’ve been making good money by investing in Lending Club (one even mentioned how it was his best investment over the past year).

They’re a company that started in mid 2007, with the following statistics:

- many thousands of investors added each month at a steady pace,

- lent out many millions to borrowers to date,

- distributed several millions in payments to investors, and

- paid several millions in interest to investors.

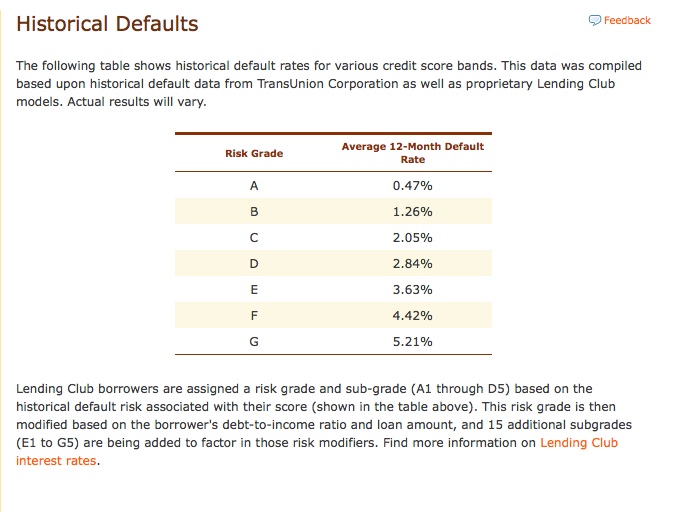

Here’s a little graphic that shows some historical statistics on Lending Club, a leading peer to peer site:

For more details on them, check out the various articles I’ve written about this company:

- Lending Club Review: A Leading Peer To Peer Lender

- Lending Club Return On Investment: Should You Invest Via Direct Lending?

- Personal Loan Interest Rates from Lending Club

Lending Club is recognized as a premier company in the peer to peer lending industry.

2. Prosper

This company’s approach to peer to peer lending used to involve a loan auction model. In the past, it operated differently from how Lending Club worked, as the latter company screens for qualified borrowers and grades loans based on a borrower’s credit risk profile. By contrast, Prosper allowed the loan network (marketplace) to set the rates through bids. Earlier on, Prosper was the 800 pound gorilla in this budding industry, thanks to a business model that was less restrictive to borrowers. While this opened the floor to more available loans in the network, there was more potential risk for default by borrowers with less favorable credit histories. Over time, this model began to erode and the problems here, coupled with the SEC imposing a quiet period upon Prosper for a certain period of time, caused the company to lose its momentum. Today, Prosper is attempting to regain its footing with a new business model that practically parallels what Lending Club is doing, and so far, the results have been positive.

This company’s approach to peer to peer lending used to involve a loan auction model. In the past, it operated differently from how Lending Club worked, as the latter company screens for qualified borrowers and grades loans based on a borrower’s credit risk profile. By contrast, Prosper allowed the loan network (marketplace) to set the rates through bids. Earlier on, Prosper was the 800 pound gorilla in this budding industry, thanks to a business model that was less restrictive to borrowers. While this opened the floor to more available loans in the network, there was more potential risk for default by borrowers with less favorable credit histories. Over time, this model began to erode and the problems here, coupled with the SEC imposing a quiet period upon Prosper for a certain period of time, caused the company to lose its momentum. Today, Prosper is attempting to regain its footing with a new business model that practically parallels what Lending Club is doing, and so far, the results have been positive.

For those of you who are interested in learning more about person to person lending or borrowing, there’s a book available on Amazon.com called “The Complete Guide To Prosper.com” that was written by Sean Bauer, a successful group leader on Prosper.com who’s well versed with the ins and outs of online personal lending in this environment.

Though I’m not much of a borrower at all, I’m looking to learn more about how to be a lender on these online social lending sites. To purchase the book, you can visit Amazon.com or Borders.com.

3. Loanio

Loanio is another player in this field, but if you visit their site, they’re in a “quiet period” right now, as they work through SEC regulatory checks (both Prosper and Lending Club have successfully passed SEC reviews already). So for now, you won’t be able to open an account or apply for a loan on their platform until further notice.

4. Pertuity Direct

Pertuity Direct started out in January of 2009 and seemed to show some promise: they offered a loan approval process that would be quicker and easier, they set the rates themselves and also performed their own credit checks. If you’re a lender, you would be investing via a mutual fund called the National Retail Fund, which invests in consumer notes that represent Pertuity Direct loans. But why am I speaking of them in the “past tense”? Because there are rumors that they’ve gone under. Supposedly, there was a shareholders’ meeting a few days ago “to approve the liquidation and distribution of all shares of the fund (National Retail Fund)”. And when I called the number on their web site to check, I was referred to Gemini Fund Management, supposedly a transfer agent for the National Retail Fund. Are they really gone? Stay tuned for the next chapter!

State of The Peer To Peer Lending Industry

The first time this “industry” came to light a few years ago, there was a lot of hoopla about just how successful and big it was going to get. With the credit crisis taking over the last few years, social lending couldn’t have come around at a better time. But as you can see, this industry is fairly new and still experiencing some challenges and growing pains.

Peer to peer lenders have been closely scrutinized by the SEC to ensure that they comply with regulations in order to protect consumers. This is not surprising, given that consumers are dealing with unsecured and uncollateralized loans with rates dictated by an open marketplace (at least in Prosper’s case). The good news is that several companies have emerged from the SEC review process and have been operating pretty successfully for a while now, with business booming!

Peer To Peer Lending Investment Returns

For now, the bigger guys (Lending Club and Prosper) are growing and appear to be doing quite well. According to Lending Club, their default rates have remained very low with their most conservative loans (the Grade A loans) having had NO defaults in recent months (click here for their historical default rates). If you’re an investor seeking to diversify beyond the boundaries of traditional investments, then peer to peer lending offers a fresh, alternative way to invest your funds.

The returns here have been pretty attractive with statistics boasting a 9.6% average annual return for Lending Club and 7.06% for Prosper. Top investors at Lending Club have managed an even higher return of between 12% to 13% a year, with individual investment loan portfolios topping $2,000,000! It’s definitely worth a look if you’re interested in a new kind of fixed income investment which can serve as a nice diversifier for your overall portfolio.

Copyright © 2009 The Digerati Life. All Rights Reserved.

{kind=link}

{ 12 comments… read them below or add one }

It is so interesting to know such network operating for investors who required money. This article opens all about the network and its full details. But, as a value investor, I strongly against borrowing money from someone for investing purpose. It is totally against my self developed investing principles and strategies. However, it is good to know how such network operating for mutual benefit, may be for sometime. Nice read.

@Sherin,

Interesting perspective. Yes, I can see how this form of investing can be against one’s principles. It’s highly acceptable in the U.S. and even the U.K. but may not be so acceptable in other cultures or other countries (depending on your outlook). I can certainly see that. The longer I’ve lived in America the more I see how much more comfortable people are with credit, debt, borrowing and lending.

I’ve been debating for a while to open a Lending Club account. Maybe just a small account to start a couple loans and see how I like the service. SVB, do you personally have an account? If so, how has your experience been?

I read on someone’s blog not long ago about how he was trying to build a passive income stream using Lending Club. Basically he was putting $50 per week I think into his account and he was so far getting about a 15% return (he was only investing in C, D, E loans) and building up the interest on the monthly payments to where he could eventually replace the $50/week from his own pocket with the interest he was receiving from the other loans. At that point, none of his own money would be going into the venture, and he would have a passive income stream that would grow on it’s own. Kind of an interesting idea if he can manage to make it work.

@Lee,

Yes, I have a Lending Club account and a Prosper Account and while I had been tinkering with p2p lending using a small diversified set of notes, I am only now starting to get into it earnestly. I am actually exploring a new feature that Lending Club has (not sure if it’s available to everyone yet) but it’s called a PRIME account. It’s an automatic way to invest. You hand Lending Club a certain amount of money, and set a target rate of return. They will then invest it for you. The thing is, that amount of money they require to start this account is on the high side ($10,000 I believe). I’m definitely debating this new way of investing with them (but of course it’s a big jump from a small investment to a $10K account, so we’ll see…).

I attended an investor’s conference at Lending Club last week and it was really fruitful. I met the LC people there and came away inspired about peer to peer lending even more. I have yet to really cover my experiences on this blog in more detail. But I intend to do so.

The strategy you describe that someone’s been trying out — very interesting. I think it’s a good idea to start small to get a good feel for it. That’s what I’ve done so far, but I’m also very intrigued by the PRIME account feature that is in the works.

The ridiculous discrepancy banks have between the interest rates they offer on investments versus the interest charged on loans has created this opportunity, and I am glad to see that there is loads of activity here. Keeping the banks out of the loop in definitely in everybody’s best financial intestest.

I think everyone agrees that social lending or P2P lending is a very interesting concept for both lenders and borrowers.

For those of you who want to learn more, I recently interviewed Lending Club’s CEO Renaud Laplanche to answer a bunch of questions that most people have about Lending Club – you can listen to that interview here.

So if you put money into a lending club can you pull your money out does it have to stay in for the life of the loan. Also is the interest rate fixed or variable. Basically I might want to put money in short term but I don’t know if that is viable.

I did some 3rd world micro lending with Kiva. But that is really more of a charity thing than an investing thing (0 percent interest). But so far no one has defaulted. It’s kind of cool.

With banks tightening their lending policies due to the economy, I’m sure peer-to-peer lending has been an asset to many people seeking microloans. As an investment it sounds like it has a lot of potential. Safer than the stock market…

I’m just about ready to give this a try. I’m glad to know it’s working for you!

Still growing this side of the Atlantic too with Zopas UK model proving more and more popular by the day and returns for me from zopa uk (after 2 years) still averaging over 8% which is way more than i can get from any savings account, although obviously the risks are greater. Good to read your overview of peer to peer lending in the States.

I’ve been investing with Lending Club for about a year now. My experience has been generally positive. It certainly beats earning a low interest rate from the bank.

One of my close friends told me how he was trying to build a passive income stream using Lending Club. Basically he was putting $30 per week I think into his account and he was so far getting about a 10% return. But this critical time, i would rather invest in physical gold and silver related assets.