How do you feel about your personal financial situation? In our case, we are going with the flow. Our financial strategy has always been to try to adjust to the current environment whenever possible. My spouse and I were long term corporate hounds and it served us well to try to climb the career ladder while investing our savings in the stock market and even in real estate for a while. That was the strategy taken by a lot of folks before Y2K hit. And it was a pretty good one for a while.

How Are Your Finances Doing? Past and Present

Well I’ve been reflecting on the 00’s decade and it’s been a lot more erratic for us. Like many people, we were slammed by the stock market roller coaster, the layoffs, the financial crisis. So our strategy has shifted. We are no longer relying exclusively on our investments as the only way to help us retire in the future. (While we are supposed to be entitled to social security income in the future, it’s something we discount altogether when we plan for our retirement. We’re just not comfortable counting on the government for these things.)

Our new approach is to see if we can focus on business — business as a way to invest in the future, rather than rely entirely on our savings and investment portfolio. Unfortunately, being your own boss has its risks, but by trying it out, we are gaining experience and learning how to think like entrepreneurs.

So how is middle America doing? How are we stacking up compared to the average American family? Are we average? In my case, from talking with my own circle of friends and family, the picture has not been so bright, sad to say. Despite improvements in the job market and with national unemployment statistics, I can still sense growing financial pressures in the lives of many families I know. For instance, here’s something I received in the mail the other day, from someone who continues to feel the pinch:

“Everyone is concerned with money. Everyone likes to earn money. But I am resigned to living the rest of my life in a simple house and not traveling around the world. I’d rather save my money to give my kids a good quality education. I never want to own a Porsche or a Mercedes. I’ll be using a Toyota Corolla or a Honda Civic until the day I die. Or maybe I’ll just use public transportation.”

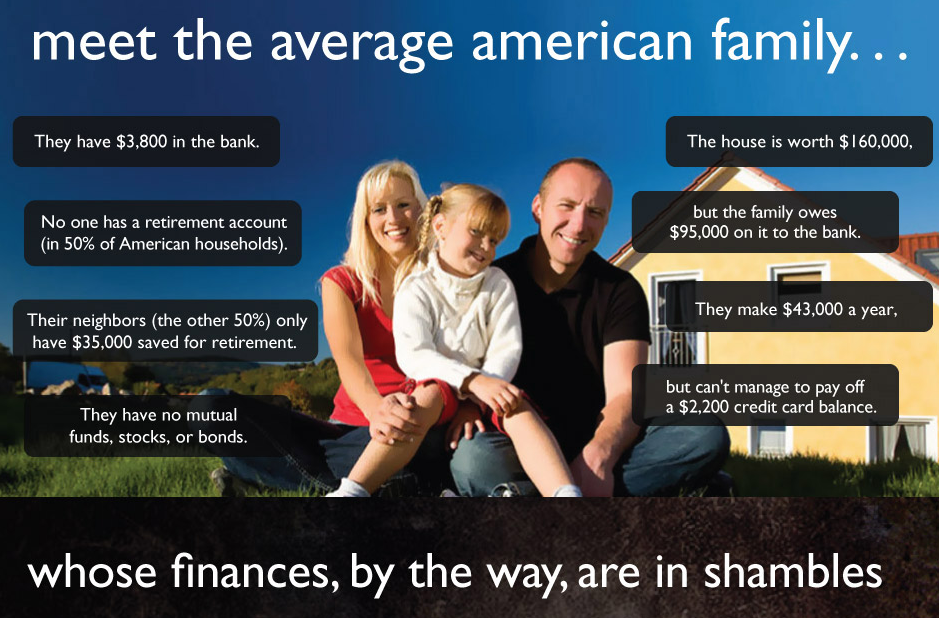

Average American Family’s Finances: In Shambles? (Infographic)

In general, America’s financial situation does not look good at all, if you’re going to take some of the facts you’ll see from VisualEconomics.com. Let’s take a look at a few statistics:

The rest of the infographic describes our “finances in shambles” (these figures are unconfirmed beyond what is shown in this image):

- The average American family has $3,800 in the bank.

- 50% of American households don’t have a retirement account.

- The 50% of households with retirement accounts only have $35,000 saved up (per family).

- The average family owns a house worth $160,000, $95,000 of which is their mortgage.

- Average income is $43,000 per year.

- Average credit card debt is $2,200.

- 40% of working Americans are not saving for retirement.

- $117,951 is the average American household’s debt.

- 25% of households have no savings whatsoever.

- 24% have postponed retirement.

- Only 18% are very confident about their retirement situation.

- $2 trillion is the combined amount of personal debt held by Americans.

- 7.7% don’t own a bank account!

Given these statistics, you may be curious about how your financial situation compares with the rest of America. Here’s a little tool to help you see how your income stacks up. Here’s how to see how your net worth measures up against your neighbors.

Copyright © 2011 The Digerati Life. All Rights Reserved.

{ 13 comments… read them below or add one }

Sounds like we’re in a bad situation. Sometimes, though, I wonder if we really are such terrible stewards of our money, or if the media just focuses on the worst statistics. I think most people try to manage their money well and have sustainable levels of debt. I also wonder how they calculated the credit card debt figure. I don’t carry a balance on my credit card, but am “technically in debt” to the tune of $1,000 to $2,000 before the payment due date. Would that also be counted?

I guess I’m just looking for reasons to be optimistic!

I guess I’m above average. We make more money, we have no consumer debt and retirement is well above $35K. Maybe it’s because I read financial blogs and books~

Across the pond it is pretty much the same story, with regard to income and debt levels and the provisions made for savings and especially retirement. I think sadly most people are feeling the ‘well if we’re all in the same boat’ effect.

Thanks for brightening my day. Whenever I’m feeling down about finances, being compared to the average family helps cheer me up.

The biggest thing that jumps out at me is that my home’s value is less than 1.5 times our household income – compared to the average family’s home being worth 3.72 times their household income. That’s a pretty telling stat when you’re looking for answers for why so many people have problems paying the mortgage.

We recently refi’d again (chopped an entire point off) and for the second time, the guy handling the refi was noticeably impressed with our credit score, considering our age (I’m 35). It was a bit of a head-scratcher for me. While we’re certainly well seated in the middle class, we’re by no means wealthy. We’re not misers, but I guess we keep our discretionary spending at a reasonable level.

Sound the alarm please, because these statistics show us where many Americans find themselves today. The state of retirement savings is very concerning.

Another statistic that helps to reveal the state of debt in this country is student loans. According to an infographic posted on eCampus Blog, the average student loan debt is $23,186 per student.

I’d like to be optimistic too and add that financial education will help us change this picture. After all, knowledge is the key to making it happen. Personal finance blogs like this one are a great way to pick up financial know-how. Thanks for sharing this post!

Thanks all. Yes, pretty unfortunate statistics. From what I remember, these numbers haven’t improved over years, but have gotten worse — no surprise, given that the last few years have been financially tough to deal with. The big issues: no savings, no retirement plan and more debt. Forget housing, the main issues, IMO are health care and student loans.

We can’t go on like this indefinitely. Something’s going to happen. In some circles, I hear that people are now getting their health care outside of the country! They go on vacation elsewhere and book their doctor’s appointments there (where it’s much more affordable). Crazy huh? My personal case is a bit better though — I’ve had on and off health problems and so far, I feel I’ve received the best care I can get. I’m happy with things.

I also realized that we truly need to try to take care of things ourselves more. In the past, I would think: oh, it’s okay to get sick, my doctor will fix me. Now I realize it’s the wrong attitude: it should be — I won’t get sick because I’ll be doing X, Y, Z and I’ll take care of myself!

Same attitude should be brought to our personal finances: Don’t think the government or even your employer is going to save you one day. Think what you can do to take care of your own.

When I look at those statistics, I think what changed. I don’t think anything changed, it has just gotten worse. Too many people are living in the present, satisfying their wants instead of their needs. The people in these situations will say they do not have any choice. Although I am in favor of increasing financial literacy, I am not sure it would change these statistics. It looks like there will be many more people working in their latter years because they are unable to retire.

The statistics are so true and with the current lifestyle we have now, more gadgets to have as necessity means more expenses for the average family and less savings.

The stats are scary, but I think you made a wise choice choosing your business as a way to invest in the future.

I can identify with the description of the American family financial shambles. I have been an IT Business Analyst for 14 years and am now faced with retraining to become a registered nurse. The fast-track degree will cost me $50,000 (too much). What choice do I have? I need a career that will hopefully be stable. If America cannot pull out of this, then my son and I will move to Sweden where life is a bit better (sad but true).

I agree with the statistics as I have been reading and researching the right financial path as I am now 40 years of age. I have been self employed for 14 years as of this blog and doing well. Of course, I have too gotten caught up in this frenzy to keep up with the Jones but have faired much better then my friends, family and colleagues. We (Wife and Kids) live in a home that is valued at 40% of my income, drive cars until they fall apart, do not try to be a trend setter however, we do take one major vacation each year to show the kids that life out side of the USA is not that bad but in some cases, better.

Based on my research the average American family is the following: Combined income of $93K, two new cars with car payment ($1200/month), $52K in Credit cards, student loans of more then $25K (Not an issue to me as it can improve your income), less than $3000 in savings, around $22K in retirement and one paycheck from the streets.

The above situation is all to common in the US and when I see people wearing designer clothes, living in a big home with brand new furniture, driving brand new cars, eating out every day I laugh because they cannot afford to go on a simple vacation outside of the city they live. It is truly sad but I blame the lack of financial education and the fact that my generation wanted their kids to have it all and by doing this we are setting them up for an even worse financial disaster.

We all need to stop and think that a few wants are OK as long as your needs are met.

Awesome numbers Doug. Glad to hear you are doing well! Our house is 30% of our net worth as well. And having it this way is a huge huge relief. I am very careful about how I spend and do not care about keeping up with the Joneses. I focus a lot of what I do on earning and “keeping” or saving, rather than on spending. Feels great!

Silicon Valley Blogger, three cheers for your comment: “Don’t think the government or even your employer is going to save you one day. Think what you can do to take care of your own.”

I’m 40 and I’m disgusted about how little I’ve learned about personal finance until just the last few years. I’m praying that I can teach my kids (my oldest is 14) how to think for themselves, avoid bad debt, create multiple streams of income, and build a secure future for themselves.