Is the economic downturn over? That’s what “they” say.

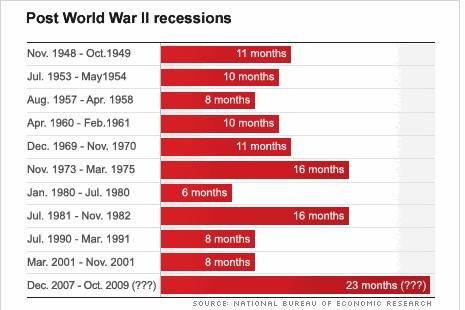

CNN Money just released an interesting slideshow about the state of the economy as of late. If you’re wondering about when (or whether) this economy will be *truly* turning around and whether your vague unsettling feelings about it have any basis, then these hard numbers should help give you perspective. If you’re going to get anything from this post, maybe it’s this: that this recession is the longest, most grating one we’ve had post World War II.

The small bit of positive news is that the economy is supposedly showing some signs of life, although the quick vote polls don’t really reflect that much enthusiasm from the citizenry just yet.

Economic Fundamentals: A Reality Check

So here’s my own commentary on the economy (based on CNN’s slideshow), which I think is still shaking off the severe hangover its been on for some time now.

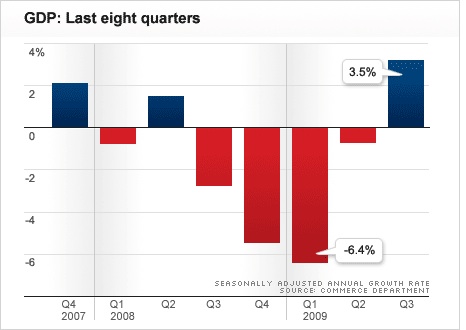

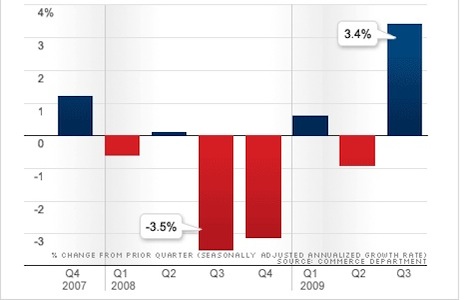

1. GDP and Economic Growth: Good

The latest growth numbers have been decent, but a lot of this may be attributed to cut backs in the business sector, layoffs, the stimulus plan, bailouts and who knows what else can be propping up our economy. So are we seeing true economic growth here? And does this justify the corresponding recovery we’re seeing in the stock market?

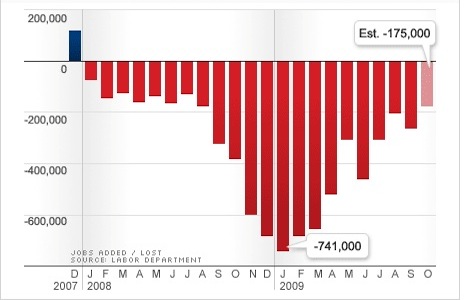

2. Jobs Situation: Slow Going

Just last week, I took a look at the national unemployment statistics and lamented the job loss numbers — which in some locales, appear to be at record highs. But here’s something to chew on: how many laid off workers are really eager to get jobs right now? Personally, I’ve encountered more than a few people enjoying unemployment benefits whilst taking their time to find “the right job” that would pay a wage they were happy with. Not that anything’s wrong with that, but it goes to show that a lot of jobs that are available today may be going unfilled (by choice) while “job searchers” pick and choose where to work or decide to sit back and collect unemployment checks while they can. Not everyone out there is desperate to take any job; there are still those who are taking their time to find just the right one.

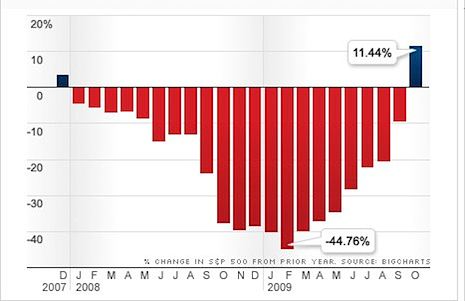

3. Stock Market: Ahead of Itself?

I still don’t get the stock market and what my online brokerage accounts are telling me: I’ve actually been making some money with my investments recently. I should be happy, right? But I’m actually still quite wary of the possibility of a double dip recession. With this market being so responsive to the good news, I hope we don’t pay too badly for what appears, in my opinion, to be premature exuberance.

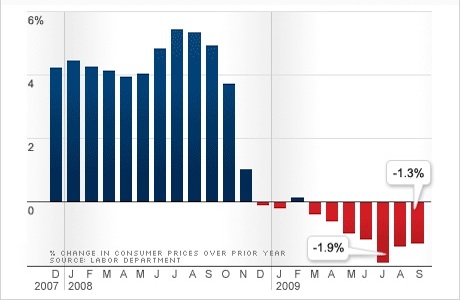

4. Inflation Watch: Okay

With the economy still in the doldrums, inflation looks tame. But economists warn that once growth picks up, inflation may become the economy’s new waterloo — which won’t be a good thing even with the small consolation of savings account rates creeping back up. This is one element of the economy that may look good now, but may shift on a dime later, when spending picks up.

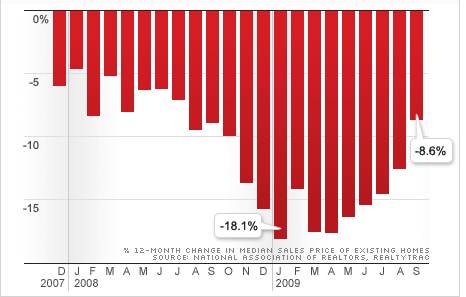

5. Housing: Spotty

Supposedly, housing is seeing a slow recovery. You can say that again. The government has tried to intervene on this front by offering relief to homeowners via tax breaks and other incentives which were folded into the last massive stimulus package. Foreclosures are up in some places, while housing prices are steady in some others: the recovery in real estate still seems spotty.

6. Spending: Slightly Improved

You can attribute some of the recent consumer spending activity to the government (Cash For Clunkers, home buyer credit, etc). But at a time like this, shouldn’t we all be watching our home budgets and pocketbooks even more? These days, it’s “hip” to be cheap!

My take on the big picture? I think a lot of what’s being reported as a “recovery” is pretty localized. For instance, I know too many people who are still out of jobs or who are working at places they wouldn’t otherwise be if they had a choice. I know a few people still worried about their debts, credit cards and housing situation. So I can only be curious about what the next several months will bring, and am wondering when the true turning point for this economy will be.

Copyright © 2009 The Digerati Life. All Rights Reserved.

{ 17 comments… read them below or add one }

“They” is us.

That’s the problem.

When you want to check whether it is raining or not, you check something objective. You put your hand out the door and if it comes back wet, you have a pretty good fix on the situation.

When you want to know whether the recession is over, you check what “they” say. Some of “they” say it’s over. Some of “they” say it’s only just begun. Both “theys” put together nice-looking charts to convince us that their “they” is the “they” that matters.

We caused the recession. And we will decide when to end it. The process by which we do that is a process in which we play all sorts of mind games with ourselves, pretending for a bit that we have decided that it’s over and then for a time that it’s only just begun and so on. We scare ourselves and then back away from the scary stuff and then try out scaring ourselves again.

The only way to get a solid fix (in my view!) is to look at something objective, something that isn’t influence by all the “theys.” This is why I look at P/E10. P/E10 is an indicator of emotion. It doesn’t give me a direct answer to the question “Is the recession over?” But it gives me an objective read of how emotional we all are being re our financial futures at this given moment. Knowing that, I have (or so I think!) at least a little bit of an objective fix on how much longer we will be playing mind games with ourselves re our financial futures.

P/E10 says today that most of us are very much still in the mind-games stage of this long process of finding our way back to a love of the reality principle.

Rob

I’m still very skeptical. I’m very hopeful but I don’t think we (the US) is quite out of the woods just yet.

Spending looks like it has GREATLY improved from the bar chart! The one thing we can never count out is the ability for the US consumer to spend, and binge again. We need binge spending to revive corporate profits higher, to therefore continue to bull market run.

I don’t think there will ever be double digit inflation in our life times. We’ve reigned in inflation, and it has been a 25 year bull market in fixed income. Output gap is still there, and inflation will remain low despite all the monetary expansion.

Jobs are coming back, and next year should be a hiring frenzy as corporates always over fire in the downturn.

Housing, give us 7 more years, I think we’ll be back to peak levels. In China, HK, Singapore, and Taiwan, housing prices are already back to their highs.

Overall, the economy feels like we’re at a rave, having a dizzying good time. Two more shots in the arm, holiday spending and year end bonuses. The true turning point in the economy was this past February, and we’ve never looked back since.

FS

If the government says everything’s OK now?

I don’t believe it!

I think the US Consumer may be the indicator, but if their spending habits are changing for the long term, it will take the economy longer to catch up with the transition. Mine is a layman’s view of course, but without jobs, and lower wages for the jobs that are out there, I wouldn’t be looking for binge spending anytime soon. Credit card companies are punishing the average person with fees, and high interest so I don’t see folks running out and buying stuff on credit either. We probably have a ways to go here and I suspect the exuberance of the market is wishful thinking.

Basically if analysts say things are better and we are done, it means we have months more. It’s hard to say its over when you still look at the unemployment rate and you ask people looking for jobs how their job search is going and they keep saying no one is hiring.

@SVB – I’m with you…skeptical. The threat of a double dip is very high considering that fiscal stimulus has a temporary effect of propping up key economic figures like GDP, consumer spending, etc. IF we are coming out of recession and IF the fiscal stimulus was enough to get consumers spending again without incentives, THEN we will wind up with a nice recovery only to run square into inflation which would trigger another recession as the Fed raises rates.

However, IF we are coming out of recession and IF the fiscal stimulus wasn’t enough to get consumers spending again without incentives, THEN we’ll have a classic double dipper.

In short, we will have another recession sooner than later and the stock market will remain choppy without making solid gains above 1999/2000 levels until AFTER we get (not this recession) the NEXT recession out of the way.

In the interim, dollar cost averaging, rebalancing, and active asset allocation will remain in favor.

From the general mood around us, it’s hard to feel optimistic about the state of the economy at this time. Even those who are doing fairly well at a time like this are feeling cautious/anxious about the future. I have to give it to Financial Samurai though, who has offered a view of the near future — hopefully it turns out as cheery as you’ve suggested:

– no double digit inflation (inflation will be controlled)

– we’ll have a hiring frenzy next year…

– 7 more years and we’ll be facing another housing peak.

Okay, please let’s just not be like Japan…. !

SVB you have developed a very unhealthy interest in double dip recessions 😉 don’t worry about it, not going to happen.

@Manshu,

I appreciate your observations 🙂 . Double dip recessions aren’t hounding me just yet — just wanted to tie in some thoughts here to past commentaries I’ve made on the economy. It seems that you are optimistic enough to rule out a relapse in the economy.

That said, do you have thoughts on the market’s behavior? If there’s nothing necessarily to fear, then I suppose a retest of market lows from earlier this year won’t be in the cards. Just surmising here, based on your comment.

The economy is still struggling big time no matter how optimists like to portray it. The increase in GDP is only because businesses have made huge cut backs and now have a lot more money to work with. I highly doubt the stimulus has had much of an effect on the GDP.

I suppose a retest of market lows from earlier this year won’t be in the cards.

If you go by the historical data, we’ll be going a lot lower than that in years to come.

That’s not a prediction. It’s a report on what the historical data says. The historical data is public information. It is available to Robert Shiller’s web site.

There are four times in history when the P/E10 value (the price of the S&P over the average of the last 10 years of earnings) went above 25. On the first three of those cases, we subsequently went to a P/E10 value of 7 or 8 because of the massive damage done to the economy when we pretended for a time that our wealth was so much greater than it really was (this is what a Bull Market is – – a national exercise in “Lets’ Pretend”). At the low earlier this year, we were at 12. We are today at 19. A drop from 19 to 7 is a long drop.

Again, I am not predicting this. It might be that there will be some reason why things will turn out different this time. I am just pointing out that this is how things turned out every earlier time this Passive Investing “idea” caught on for a time. People should know that this is a live possibility (I view it as a strong probability given that we have never seen anything different anytime in the historical record) and plan accordingly.

I do not believe we should be wishing for higher stock prices. Higher stock prices increase the chances of a second crash, which would probably send us into the Second Great Depression. I was hoping that valuations would stabilize back when we were at 12. If we had stayed at 12 for several years, we could have avoided a second crash and earned 6.5 real on our stocks while doing it (that’s what we earn when the P/E10 number is stable). Things did not turn out that way and I see that as a very dark development indeed.

Rob

Hi Rob! Would you care to wager we will NOT breach S&P500 666, or this years March lows over the next 12 months? Heck, I’ll even give you 24 months or whatever amount of time you need to take the other side of the bet.

By any chance did you capitulate at the bottom? I don’t understand why you have so much negativity. Think positively, you’ll feel better!

Would you care to wager we will NOT breach S&P500 666, or this years March lows over the next 12 months? Heck, I’ll even give you 24 months or whatever amount of time you need to take the other side of the bet.

There’s a sense in which we’re all taking a wager when we set our stock allocations. That’s what it’s all about. We look at the situation, assess the probabilities, and aim to get on the side that is likely to pay off. We all do that, all the time. The difference between Passive Investing and Rational Investing is that Rational Investors consider the probabilities of various outcomes before placing their bets. I think that makes sense.

If I were betting, this is how I would state my view: “There is a 75 percent chance that we will go to a P/E10 level lower than 12 within the next four years.” I don’t believe that it is possible to make short-term predictions effectively and I don’t believe that even long-term predictions can be precise. But I do believe that the historical data can be used to make long-term predictions that are close enough to the mark to help you know when to make shifts in your stock allocation.

If you believe the above assessment, you might want to have 35 percent or 40 percent in stocks today, but probably not much more than that. My view is that stocks offer a better long-term bet today than they did prior to the crash but that stocks do not now offer an exciting long-term value proposition (I wouldn’t have said that during that short period of time when prices had worked their way back down to reasonable levels).

By any chance did you capitulate at the bottom?

No. I got out of stocks in the Summer of 1996. Prices went to insanely dangerous levels in 1996 (meaning that the long-term value proposition was poor) and did not return to reasonable levels until late last year and then only briefly. I am ahead on that 1996 “bet,” by the way. My money was in TIPS and IBonds paying 3.5 percent real for that entire time-period. By investing that money in stocks at reasonable prices (and receiving the great long-term return that follows from doing that), I can increase the amount by which I am now ahead by more and more as the years pass.

Timing has gotten a bad name because most people hear the word “timing” and think “short-term timing.” It is true that stock returns are not predictable in the short term and that, thus, short-term timing is a bad idea. But long-term timing has to work. It is not even possible for the rational human mind to imagine a scenario in which prices would stop affecting long-term returns. As long as you don’t get too greedy and try to predict long-term returns too precisely (precision is not possible even in the long term), there is no way that long-term timing can let you down. It gives you higher returns at lower risk, the best of both worlds. It has worked for as far back as records of stock prices are available.

I don’t understand why you have so much negativity. Think positively, you’ll feel better!

Would you call it negativity if I said that I like to look at the price of a car I buy before putting money on the table? Where did this idea come from that it is somehow “negative” to want to get a decent return when buying stocks? I take price into account when I buy everything else I buy, and I bet you do too. So why not stocks?

Have you ever stopped to consider how much money you will be putting into stocks over the course of your life? If you are frugal on every other purchase you make and spendthrift when it comes to stocks (to invest passively is to ignore price and that is a spendthrift approach), the gains you will obtain from being spendthrift re stocks will cancel out the gains you obtain from being frugal on every other purchase.

I have checked the historical data to see how many years earlier we could all retire by paying attention to price when buying stocks. The answer is — we could all retire five years sooner. That should not be surprising. Paying attention to price in all other areas helps us retire early, does it not? Stocks are just like anything else you can buy in that with stocks too price matters.

Where does the negativity come in? I see this approach as a 100 percent positive one. It’s a win/win/win/win/win.

Rob

Rob,

Will you bet on S&P breaching the low of 666, yes or no? PE is too vague bc who’s to say what 10X is? 666 it is. Let’s bet!

I’m impressed you got out and stayed out since 1996! I was a fun run in 99-01 and a lot of fortunes were made.

Will you bet on S&P breaching the low of 666, yes or no?

I can give you a rough sense of the probabilities that this will happen, Samurai. I cannot offer a guaranty. My view is that we should all take the probabilities into account when setting our allocations. That’s taking a bet, in one sense of the phrase. But it is also taking a bet to not determine the probabilities. They are just different sorts of bets. My view is that I am taking better-informed bets (but I would imagine that those who follow other practices also believe that their approach is the better-informed one).

PE is too vague bc who’s to say what 10X is? 666 it is.

I don’t understand this comment. The “10” in P/E10 is the average of the last 10 years of earnings of the S&P index. It’s a numerical calculation. Anyone who goes to the trouble of calculating it (or reading of someone else’s calculation) knows what it is. There is nothing vague about it.

I’m impressed you got out and stayed out since 1996!

It’s kind of you to say that, Samurai. I can assure you that I took a lot of heat for it too! Each time I would feel heat, I would review the historical data again to build up my confidence. My view is that the only way we can develop true confidence in our investment decisions is to root them in something objective.

I think it’s interesting that the Passives agree with me on this. They too root their strategies in something objective — the market price. The difference is that they believe that the unadjusted market price is right and I believe that the market price as adjusted for valuations is right. That’s the only difference between the two approaches (but the strategic differences that result from that one distinction are huge).

The reason why I feel we need to adjust the market price for valuations is that by definition the market price is wrong to the extent we experience either overvaluation or undervaluation. If the market were valued properly (as the Passives assume is always the case), there could not be overvaluation because overvaluation is always a mispricing. When you hear the phrase “you can’t beat the market,” you should reply “Of course I can! — at times when the market is mispriced.” At times when the market is priced reasonably, it is true that you cannot beat it. To find out whether it is possible to beat the market at a given time, you need to determine how much mispricing is present at the time. This is what P/E10 tells you.

I was a fun run in 99-01 and a lot of fortunes were made.

Fortunes are made in lottery tickets every day. It doesn’t follow that I should invest my retirement money in them or that I should urge others to do so.

The “run” of the late 1990s is the cause of today’s economic crisis. We are today paying back to ourselves the money we borrowed from our future selves when we pretended for a time that stocks were worth the insane prices for which they were selling in the late 1990s. Passive Investing is akin to using credit cards to buy all kinds of toys that you cannot afford to buy with real money. Yes, it seems like fun at the time. But the bill always comes due with interest sooner or later.

Today we are seeing many failed retirements, many failed businesses, and many failed marriages as a result of that “fun run.” I mean no personal offense, Samurai, but I don’t get the joke. My hope is that we will get to a point at which we will all unite in a desire to do something about the financial misery we cause ourselves with our “belief” (does anyone really believe on a deep level that the conventional investing advice makes sense?) that prices matter for every thing on Planet Earth that we spend money on except the thing that we spend the most money on during the course of our lives — the stocks we buy to finance our retirements.

Rob

I think…. the figures don’t really shows you the hard facts. Cause I was talking a stroll down the street one fine morning and realized that so many business has gone bankrupt and so many of these closed and closing store and still the government says that we are recovering. I wonder that the facts that figure tells are faraway from reality.